Yann Furic

B.B.A., M. Sc., CFA®

Senior Portfolio Manager, Asset Allocation and Alternative Strategies

The confinement continues…

Pending the global flattening of the COVID-19 curve, the global economy is still on hold.

The almost complete shutdown of the economy has given rise to fiscal and monetary measures of unprecedented speed and scope. At the same time, unemployment claims in Canada and the United States are at an all-time high.

Winners and losers

Some industries are doing better than others: shares of companies involved in containment or telework have declined less sharply than the overall market, and some have even risen. This explains why a technology index like the Nasdaq has done better than the S&P 500.

Businesses in the recreation, restaurant, travel and cruise industries are all down sharply and are expected to experience the negative effects of border closures and social distancing. This is the case for many restaurants, which will not be able to cover their costs if their establishments have to comply with distancing standards. The same applies to bars and stadiums.

Again, quality companies with no debt problems should fare better.

The stock market

Equity markets have recovered almost half of their losses, as have bond market credit spreads which, after widening sharply (falling prices), have now started to narrow (rising prices). Stock markets are looking ahead, and investors expect an economic recovery later this year and in 2021, thanks to fiscal and monetary programs.

Note that stock markets are not always representative of a country’s economy. For example, the energy, materials, industrials and real estate income trust sectors represent only 16% of the S&P 500, while the technology, consumer staples, telecommunications and health care sectors make up 59% of this index.

Oil again

The price war between Russia and Saudi Arabia, as well as the sharp drop in demand due to containment measures, continues to put downward pressure on the price of oil which, on April 20, reached an unprecedented negative price per barrel. The current drop in global demand of 35 million barrels per day is equivalent to around 35% of daily pre-pandemic demand. Short of money, oil companies are laying off their employees.

When will the recovery begin?

In the case of certain European countries such as Germany and Denmark, there are plans to open schools and certain businesses soon. In Quebec, residential construction has partially resumed.

To reduce the risk of a second wave, there is a consensus that deconfinement should be gradual. Pending a vaccine – which should take 12 to 18 months to develop according to estimates, an increased capacity to test the population remains a necessary condition for the reduction of government protection and social distancing measures.

But what type of recovery?

There are recoveries and … recoveries!

In fact, there are four different types, according to economists.

Let’s take a closer look.

- The V-shaped economic recovery: a rapid recovery following a rapid decline

- The slower U-shaped recovery

- The even weaker L-shaped recovery

- The W-shaped recovery, with not one but two declines

These letters stand for the shape of the graph showing the levels reached by the stock market indices. At present, economists believe that the coming recovery will likely be in the form of a U or an L.

V-shaped recovery

At the start of the crisis, various specialists expected a V-shaped recovery, characterized by a rapid recovery, immediately following an equally precipitous decline. In economic terms, this type of recovery could mean a return to pre-crisis levels by late 2020.

The 2008 financial crisis is a perfect example of this type of recovery.

- On the stock market, we witnessed a rapid decline in various indices such as the S&P/TSX, which ended on March 9, 2009.

- The market then began a strong and sustained recovery ending in February 2020. This bull market was the longest in history.

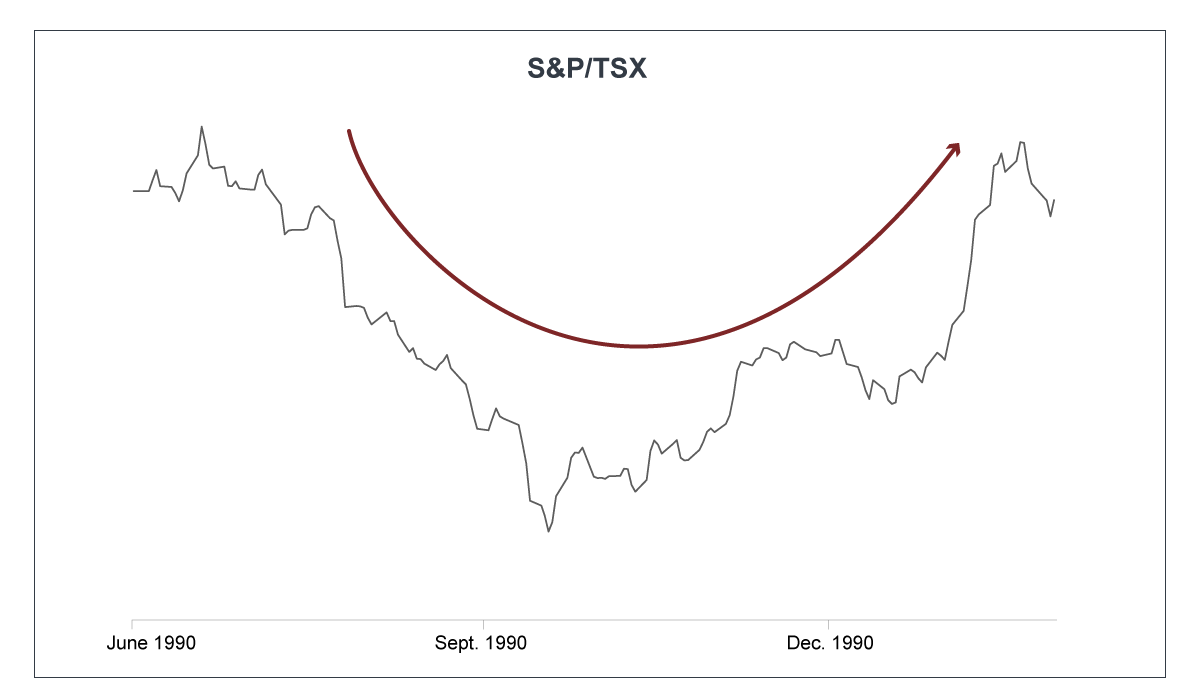

U-shaped pause

The second type is a U-shaped recovery. The stock market decline following the outbreak of the Persian Gulf War in 1990 is a good example of such a recovery, although the Canadian stock market was not officially classified as a bear market. A bear market is characterized by a decline of at least 20%, while the Canadian stock market fell by only 16.5%.

- U-shaped recovery is marked by a longer trough.

- This phase is followed by a more gradual rise, so it takes slightly longer to return to pre-crisis levels.

In economic terms, such a recovery would mean a return to pre-crisis levels in 2021.

W-shaped double bottom

And then there’s the W-shaped recovery, with not one but two bottoms before a sustainable recovery. The technology crisis of the early 2000s took this form.

- A first low was reached in September 2001, followed by a stock market rebound of more than 23% until March 2002.

- The market then began a second phase of decline until October 9, 2002, the real bottom of the crisis.

This type of recovery would postpone the return to normal by several months. It is precisely for this reason that the re-opening of the economy must be done gradually, in order to avoid a second strong wave of contagion.

L-shaped or long recovery

Finally, there is the L shape.

/ In this type of recovery, the return to pre-crisis levels takes a very long time to achieve and can take several years.

Which type of recovery will this be?

Several factors influence the form that the recovery will take:

- the nature and severity of the trigger for the crisis

- the strength and duration of the stock market decline

- the government and central bank response

Most countries around the world have implemented exceptional containment measures, lowered interest rates and injected massive amounts of money to support businesses and individuals. Everything is in place to foster a return to normal.

Last week, the American firm J.P. Morgan published its projections:

- V ➔ 30% chance

- U ➔ 55% chance

- L ➔ only a 15% chance

Only time will tell. However, the Financial’s investment team is monitoring developments very closely and constantly adjusting its strategies in order to best capitalize on the situation that emerges.

If you have any questions about your investment portfolio, feel free to contact your advisor. We’re working hard to protect your assets during this difficult time. You can count on us.

Yann Furic, B.B.A., M. Sc., CFA

Senior Portfolio Manager, Asset Allocation and Alternatives Strategies

Stéphane Girard, MBA, CIMTM, Fin.Pl.

Product Manager, Professional Practice

The information contained herein has been obtained from sources deemed reliable, but we do not guarantee the accuracy of this information, and it may be incomplete. The opinions expressed are based upon our analysis and interpretation of this information and are not to be construed as a recommendation. For any questions, don’t hesitate to contact your wealth management advisor or your tax specialist, accountant or legal advisor.