The year 2018 was particularly difficult for investors, the stock market decline in late December marking the worst year-end since the 2008 crisis. The political and economic headlines only added to the gloomy sentiment. Investors, falling prey to worry and confusion, are still unsure of what actions to take.

Should they give in to panic, or step back and consider the situation from a broader historical perspective? Looking at past financial crises, what lessons did they teach us about how to act in this environment? And how has the Financial integrated these teachings into its investment philosophy and the construction of its portfolios?

Ten years already!

A decade has passed since the 2008 financial crisis, which triggered the biggest stock market decline since the Great Depression of the 1930s. In Canada, the S&P/TSX Index lost 44% of its value between May 2008 and February 2009, when the bottom of 8,125 points was hit.1

This bear market caused many investors to question their goals, their strategies and how much volatility they were prepared to tolerate in their portfolio. Many panicked and sold all their investments. The Investment Funds Institute of Canada (IFIC) reports that net investments (purchases minus redemptions) in mutual funds fell to $0.1 billion in 2008 and $1.5 billion in 2009, versus close to $35 billion in 2017.2

1 Bloomberg.

2 INVESTMENT INSTITUTE OF CANADA (IFIC), IFIC Industry Overview, January 2018

The lessons of 2008

Admittedly, the 2008 crisis taught us many lessons and some key basic principles. We want to share them with you so that you can view the current situation in a new light. They may help you to put things in perspective and to see how stock market cycles evolve and, especially, how to react to them.

Principle 1 – Stick to your long-term objectives

What have been the repercussions of the investment decisions made over the past ten years? The chart below shows the value of the investments of three investors in Canadian stocks who made very different decisions on January 1, 2009.

Source: Professionals’ Financial; data from Bloomberg and Statistics Canada.

- The first investor remained invested, confident that his investment policy would enable him to achieve his long-term financial goals. The value of his portfolio rose from $100,000 in January 2009 to $214,228 on December 31, 2018.

- The second investor decided to temporarily exit the stock market and wait for the storm to pass before reinvesting. He sold his portfolio of Canadian stocks on January 1, 2009 and invested $100,000 in a guaranteed investment certificate at 2%, before finally re-entering the market on January 1, 2010. Despite his efforts to limit his losses, this investor is nevertheless more than $52,000 behind the investor who stuck to his strategy.

- The last investor capitulated and sold all his stocks. He turned to 5-year guaranteed investment certificates. Assuming that the rate of return on these certificates was 3%, this investor’s portfolio is worth $134,392 today.

The chart clearly shows that entering and exiting the market can be costly. It is extremely difficult to perfectly time buying and selling, as evidenced by the study conducted by Fidelity Investments which showed that, five years after the 2008 financial crisis, 25% of investors had still not re-entered the stock market.3

3 FIDELITY INVESTMENTS, Lessons Learned 10 Years After the Global Financial Crisis Serve as Powerful Reminders for Investors, October 26, 2017.

Principle 2 – Manage risk with diversification

Many studies show that diversification is the key to investing. When a portfolio is constructed according to the maximum volatility that an investor can tolerate and incorporates excellent diversification, the investor can weather any storm. A study by Brinson, Singer and Beebower4 showed that more than 91% of the return and stability of an investment portfolio can be attributed to its diversification. So the construction of a portfolio must be carefully planned.

4 BRINSON Cary P., SINGER Brian D., BEEBOWER Gilbert L., Determinants of Portfolio Performance II: An Update, 1991, Financial Analysts Journal.

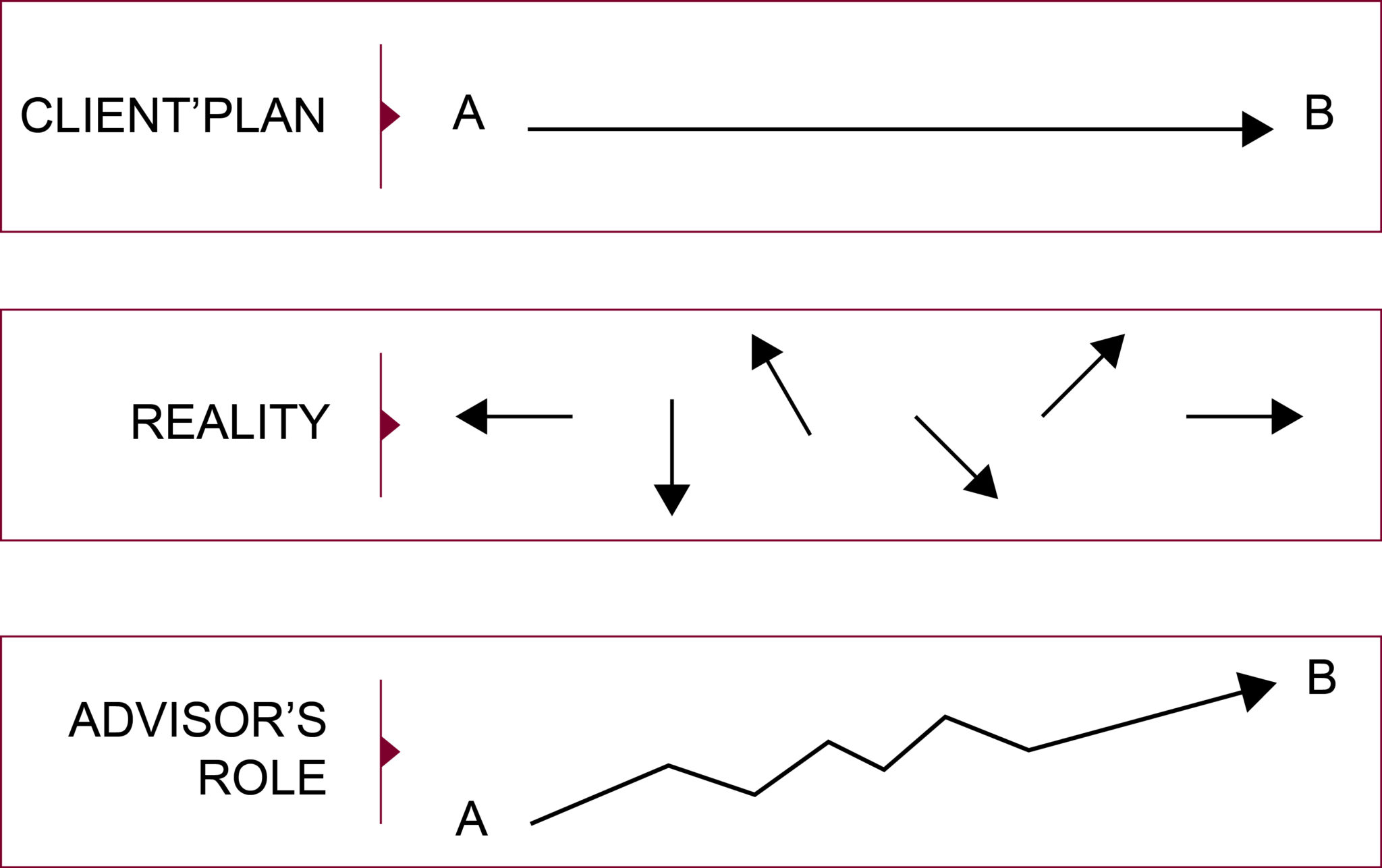

Principle 3 – Consult your advisor

Making sound investment choices is no easy task. Fortunately, your Professionals’ Financial advisor is there to help you. According to the above-mentioned Fidelity Investments study, 50% of investors who have a financial advisor feel more confident about their current investment approach than they did 10 years ago, versus only 31% for investors without an advisor5. The IFIC also showed that people who deal with an advisor accumulate on average 3.9 times more wealth after 15 years than investors without an advisor6. As the chart below illustrates, your advisor helps you to stay the course and to achieve your financial goals by making sure you get from point A to point B.

5 FIDELITY INVESTMENTS, idem.

6 INVESTMENT INSTITUTE OF CANADA, idem.

Source: Professionals’ Financial

Acting to protect

Considering the decisive role that your wealth plays in both your financial plan and your retirement plan, we have drawn lessons from the last financial crisis and used them in developing our portfolios and our Private Management approaches.

Through well-considered and targeted actions

As the manager of your assets, our investment team is involved in a process of continuous analysis in order to implement the most effective measures to protect your portfolio. Over the past decade, structural adjustments were made to avoid hasty and emotional reactions when market conditions are less favourable.

- Creation of two new private management approaches, one of which focuses on income to reduce risk, generates more current income and a higher dividend yield, and is composed of less volatile securities (2010).

- Adoption of a more global international equities approach for greater flexibility in the geographic choice of securities (2012).

- Reduction of our Canadian equities strategic weighting for better investment diversification in international equities.

- Greater exposure to foreign currencies, including the U.S. dollar and the Japanese yen, two safe haven currencies in times of crisis. (An effective decision considering the loonie’s 8% drop in 2018.)

- Review of our external manager selection process: the skills sought concern quality stock selection and reduction of volatility, particularly during market pullbacks.

- Addition of an alternative investment strategy which is less correlated with traditional assets and which seeks to reduce volatility during periods of market fluctuation (2015).

- Selection of new Canadian equity managers whose investment style offers better protection in bear markets (2017). They also have greater flexibility and can maintain higher cash levels when appropriate, which provides additional protection.

Through well-constructed funds

The considerable work done over the years to improve our range of mutual funds paid off in 2018.7 More than 80% of our funds were ranked in the first or second quartile of their category and generated a return that exceeded the median in their respective category by a percentage of up to 3.83%8. In all of our equity mandates, our portfolio returns beat their benchmark indexes by 1% to 3% in the fourth quarter8.

For example, let’s look at the performance our FDP Balanced Portfolio Series A:

- Return 19% above the median in its category in 20188.

- At the height of the crisis (from May 2008 to February 2009), the value of an investment in the fund decreased by 56% versus 44% for an investment in Canadian equities alone (S&P/TSX Composite)8.

- An investor who kept $100,000 in the FDP Balanced Portfolio from January 2009 to date would today have an investment worth $178,000, compared with an investor who exited the market for one year before re-entering (total value of his portfolio now: $161,769)8.

The diversification of the FDP Balanced Portfolio easily beats any illusory attempts to time the market.

7 At December 31, 2018.

8 Source: Morning Star.

A final word: team up with your advisor!

Professionals’ Financial was created to protect the wealth of professionals and that is what we continue to do, on a daily basis. So don’t hesitate to discuss your situation with your advisor and ask him your questions: he’s an expert who knows you well and who works for you. Establish with him a strategy that you are comfortable with and that responds to your needs. Regardless of the market situation, you’ll be able to stay the course with confidence!

François Landry , CFA , CFA

Senior Vice-President and Chief Investment Officer |

François Lavoie , B.A.A., B. A., Adm. A, F. Pl. , B.A.A., B. A., Adm. A, F. Pl.

Senior Vice-President, Wealth Management |

Professionals’ Financial – Mutual Funds Inc. and Professionals’ Financial – Private Management Inc. are wholly owned by Professionals’ Financial Inc. Professionals’ Financial – Mutual Funds Inc. is a portfolio manager and a mutual fund dealer which manages the funds of its family of funds and which offers financial planning advisory services. Professionals’ Financial – Private Management Inc. is an investment dealer member of the Investment Industry Regulatory Organization of Canada (CIRO) and the Canadian Investor Protection Fund (CIPF) which offers portfolio management services.

Commissions, trailing commissions, management fees and expenses all may be associated with investments. The indicated rates of return are the historical annual compounded total returns, including changes in portfolio value and reinvestment of all distributions, but do not take into account sales, redemption, distribution or optional charges or income taxes payable by an investor that would have reduced returns. Rates of return are calculated according to the modified Dietz method. Comparisons with indices may vary according to the portfolio size, investment timing, and mandate objective. Please read the prospectus before investing.