Plan for the unexpected

You’re in school or starting your career and you have your future ahead of you… unless something unexpected occurs. Accidents, illness or other difficult situations can have significant financial consequences for you. That’s why it’s important to have insurance.

Identify your needs

The impact of financial risks and, consequently, the need to insure those risks vary greatly depending on your situation and your obligations. Your insurance needs also change when you go from one stage of life to the next.

Understand the risks

The key is to make sure you have sufficient coverage, from both a personal and a professional standpoint, in terms of life insurance, disability insurance, prescription drug insurance, and property insurance.

Risk, frequency and seriousness

When identifying your needs, the types of risks are a decisive factor. Insurers assess the benefits required to maintain your standard of living and that of your dependents or your partners, as well as the benefits required to pay off your creditors.

| Risk | Frequency | Seriousness |

|---|---|---|

| Home fire | Low | High |

| Prescription drug claim | High | Low |

| Sick day | High | Low |

| Long-term disability | ||

|

Low | High |

|

High | Low |

| Death | ||

|

Low | High |

|

Low | High |

|

High | Low |

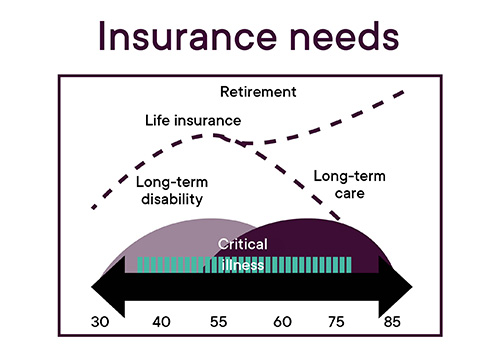

Changing needs

Changing needs

Your insurance needs change according to your age and your life stage. For example, at the beginning of your life, you don’t earn any income and you have no dependents. Your need for replacement income is nil since you depend entirely on your parents.

At the beginning of your career

The situation is very different at the beginning of your career.

- Your needs generally exceed your income.

- You have to borrow.

- Your net worth is minimal or negative, and many debts have to be repaid at the same time (student loan, car loan, mortgage, etc.).

- Your assets are not very diversified and your home is often your main asset.

- You may have young children.

Good protection

Your priority will thus be to establish an emergency fund to protect yourself and your family in case of disability or death. It is at this stage that your personal needs for life insurance and disability insurance are generally the greatest.

Disability insurance

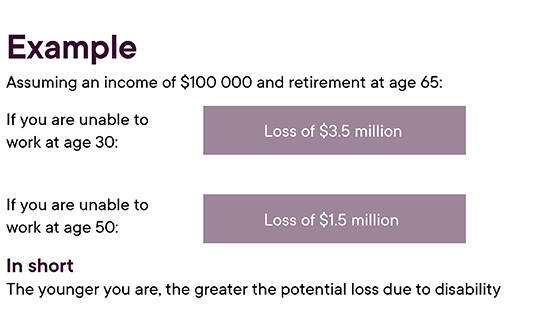

Disability insurance enables you to maintain your standard of living if you become unable to work. Since at a young age the risk of developing a long-term disability is greater than the risk of death, it’s very important to have sufficient disability coverage. In fact, this type of protection is important until you achieve financial independence.

To live normally

Regular disability benefits will enable you to cover:

- Your living expenses

- Your recreation expenses

- Your additional disability-related needs

- The cost of your investments for retirement

«Salary insurance»

Your monthly benefit will depend on a number of factors, including your income and your retirement savings needs. It’s important to verify several points before buying a disability insurance policy:

- The definitions of total disability and partial disability

- Exclusions:

- Some policies provide for benefits only if you are unable to work in any field whatsoever.

- Others pay benefits if you are unable to practise your profession.

- The benefit payment period runs until the age specified in the contract.

- Indexing of your benefits to inflation.

Life insurance

Death at a normal age (according to life expectancy) should not jeopardize the financial situation of your survivors, save for a few rare exceptions. Different types of products cover specific needs.

Types of life insurance products

| Temporary

Covers often substantial temporary needs at a low cost |

|

| Examples of temporary needs | |

|

|

| Permanent

Covers permanent needs |

|

| Examples of permanent needs | |

|

|

Critical illness insurance

This insurance pays a non-taxable lump-sum benefit of $25,000 to $1 million. Generally, this amount is paid if you survive 30 days after the diagnosis of a critical illness covered under your contract.

Your recovery

The benefit enhances your quality of life. It enables you to obtain better, priority treatment and to avoid ruining your retirement plan by having to withdraw funds from your RRSP, which would be taxed at a rate of 53.31%.

It reduces stress and eases financial strain, thereby allowing you to focus on your recovery.

Risk management

Your insurance portfolio should be reviewed regularly. It is an integral part of a sound personal financial plan.

When to buy?

These major life events are generally a good time to consider insurance:

- Birth of a child or grandchildren

- Marriage or divorce

- Death of a parent or a spouse

- Children leaving home to study or to start a family

- Purchase of a home or a cottage

- New job or business start-up

These are opportunities to review your insurance needs and, above all, to make sure your needs are fully covered.

Be informed

Make your life easier

fdp Private Wealth Management gives you access to all the resources you need to help you make the best choices. In collaboration with our affiliated companies in the insurance field, our professionals have the necessary expertise to guide you and assist you.

Professionals you can trust

For more detailed answers and a thorough analysis of your situation, place your trust in one of our advisors.