Yann Furic

B.B.A., M. Sc., CFA®

Senior Portfolio Manager, Asset Allocation and Alternative Strategies

The conflict with Iran and the resulting blockade of the Strait of Hormuz are having negative impacts on the price of oil and its derivatives, on the availability of fertilizers, and on many other products that transit through this crucial waterway.

Iran’s largest trading partner, China, has openly pressured Iran to continue negotiating with the United States, primarily to allow for the resumption of unrestricted maritime trade in the region.

Will oil prices fall soon?

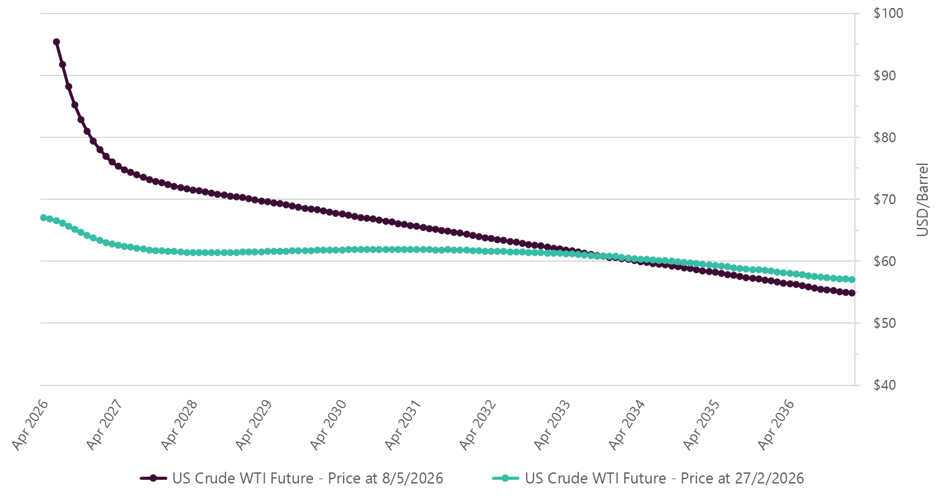

As for oil, investors believe the Strait of Hormuz will reopen sooner rather than later. This expectation is reflected in futures prices, which are expected to settle in a range of US$75 to US$80 per barrel over the coming months, whereas on May 13, the price was US$102.9.

The following chart shows how oil prices will evolve according to two scenarios:

- The purple line represents the prices expected at the close of trading on May 7, that is, after the conflict began.

- The turquoise line represents the prices expected before the conflict began.

- WTI is the benchmark price for oil in the United States.

Here are the reasons why oil prices are expected to remain high in the long term:

- Restarting certain oil wells may take time and limit the recovery in supply.

- Some countries are buying more oil to replenish their reserves, which is increasing demand.

- A “geopolitical” premium persists, meaning that international tensions are putting upward pressure on prices as market participants anticipate potential risks.

In summary, even though the conflict has changed the outlook, several factors will keep oil prices high, according to forecasts.

Corporate earnings on the rise

Yet, despite the uncertainty caused by the conflict, corporate earnings continue to rise.

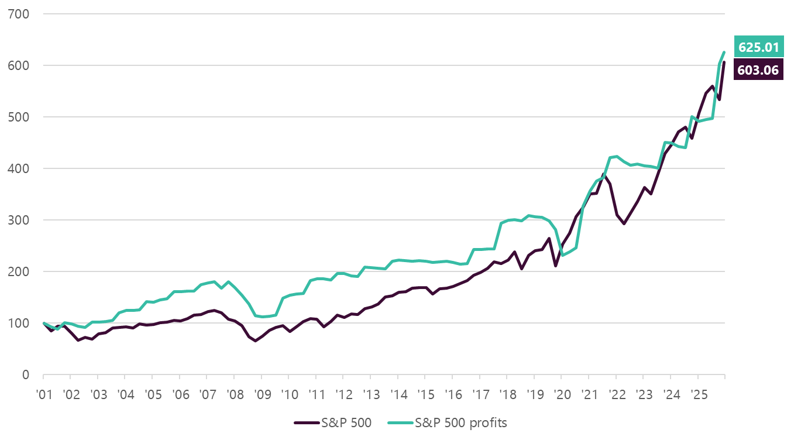

Stock market indices react to expected earnings per share. For example, over the past 25 years, the earnings of the companies included in the S&P 500 index have increased by 625%, while the index itself has risen by 603%.

This means that even though the economic environment is challenging, robust earnings are keeping stock market indices strong and driving their continued rise. Investors are therefore continuing to bet on companies’ future growth.

What’s driving the indices higher

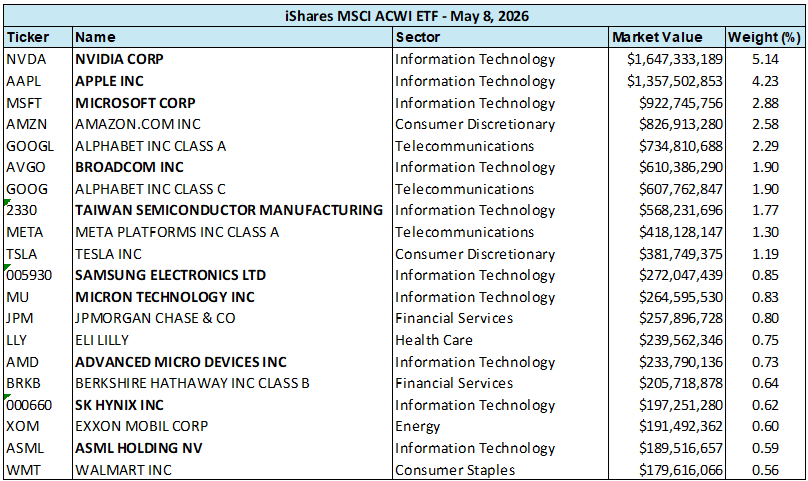

In the case of the S&P Index, it is the major technology companies and the deployment of artificial intelligence that are significantly boosting corporate earnings across the entire index. In recent years, these technology companies have also had significant weight in the index—not only in the U.S. index but also in the global index, which includes emerging markets.

Among the twenty largest global market caps, 13 are related to technology and artificial intelligence, and the number rises to 14 if Tesla is included.

To summarize the situation, investors’ expectations of a swift resolution to the conflict, coupled with steady growth in corporate earnings, have driven several stock market indices to new record highs.

However, consumer confidence is beginning to waver, and global economic activity is showing signs of slowing.

It is becoming increasingly clear that a complete closure of the Strait of Hormuz for several months would have negative effects on the global economy as a whole and, by extension, on corporate earnings.

For you, investors

Recent weeks have shown that it is difficult to predict market fluctuations, while periods of greater volatility point up the importance of structured and disciplined management.

Although the news published in the media can be alarming at times, the key is to stick to your investment strategy.

If you have any questions, don’t hesitate to contact your advisor to discuss your situation.

Financial market performance last month

OVERVIEW OF GLOBAL EQUITY MARKETSAll percentages are in Canadian dollars. |

||||

|

Country |

Index |

Return* |

Change |

Year-to-date return in 2026 |

|

Canada |

S&P/TSX |

3.81% |

|

7.90% |

|

United States |

S&P 500 |

7.77% |

|

4.96% |

|

|

Nasdaq |

12.47% |

|

6.53% |

|

International stock markets |

EAFE |

4.80% |

|

5.37% |

|

Emerging markets |

|

11.88% |

|

13.72% |

|

China |

MSCI China |

1.08% |

|

-6.29% |

*The return shown is the total return, which includes the reinvestment of income and capital gains distributions

Source : Morningstar Direct.

RETURN ON CANADIAN BONDS |

|

| Index | Return from January 1 to April 30, 2026 |

| FTSE Canada Universe Bond Index | 0.12% |

Source : Morningstar Direct

Data influencing the markets

CANADA |

UNITED STATES |

Recession Indicator |

|

Moderate |

Moderate |

Policy Rates |

|

2.25% |

3.50% – 3.75% |

|

No change was announced by the Bank of Canada on April 29, 2026. According to the BoC, GDP growth is expected to remain positive in 2026. |

The U.S. Federal Reserve kept its policy rates unchanged on April 29, 2026. Uncertainty surrounding inflation and employment persists and is compounded by inflationary pressures stemming from the conflict with Iran. |

Employment Situation |

|

|

Jobs lost: 17,000 Expectations: gain of 10,000 |

Jobs gained: 115,000 Expectations: gain of 65,000 |

|

|

|

|

Wage growth: 4.8% Expectations: 4.7% |

Wage growth: 3.6% Expectations: 3.8% |

|

Unemployment rate: 6.9% Expectations: 6.7% |

Unemployment rate: 4.3% Stable: No change |

Inflation |

|

|

April: 2.8% Change: +0.4% |

April: 3.8% Change: +0.5% |

Overall, what are the economic indicators telling us?

Benchmark rates (Canada, Europe and the United States) ![]()

- U.S. Federal Reserve: no change in rates in April, with no rate cuts expected in 2026, though nothing is certain. A new chair has been appointed and is expected to take office in the coming months.

- Bank of Canada: no change in rates in April, with close monitoring of the consequences of the conflict in Iran. One or two rate hikes are possible over the next year.

- European Central Bank: on hold and awaiting future economic data. Expectations of two or three rate hikes this year due to the conflict in Iran and its impact on energy prices.

Global Purchasing Managers’ Index ![]()

- Manufacturing segment: positive, with 24 of the 30 countries in this segment posting a reading above 50 (expansion).

- Services segment: continues to hold up but weakened significantly over the past month.

Inflation rate ![]()

- Overall: Concerns are emerging about a rise in inflation due to the conflict with Iran and energy prices. General trend: Rates are expected to remain unchanged or rise.

Factors to watch

- Conflict with Iran: The global tensions it is causing, and especially the duration of the closure of the Strait of Hormuz, will have an impact on corporate earnings. The longer the conflict drags on, the greater its repercussions will be.

- Deregulation in various industries in the United States: this should help maintain economic growth and encourage investment. Other countries, such as Canada, will have to follow suit or risk losing competitiveness.

- Trade tensions: Supported by the indiscriminate use of tariffs, they could cause an economic slowdown and increase inflation. This situation could lead to an episode of stagflation, the most negative economic scenario. The trade agreement between Canada, the United States and Mexico (CUSMA) will have to be renegotiated in 2026.

- Inflationary scenarios: If they result in keeping yields on five-to-ten-year maturities at high levels, they should be avoided at all costs, as they would slow business investment and the reshoring of production lines to the United States.

- Geopolitical uncertainty: Conflict between the United States and Iran, the Russia-Ukraine war, regional conflicts in the Middle East, tensions between the U.S. and China, possible annexation of Taiwan by the Chinese government, return of the Monroe Doctrine in the United States.

fdp tactical views – April 2026

- We increased the equity weighting in the tactical allocation strategy in all geographies.

- Economies continue to grow. Large companies are generally reporting solid earnings, which is keeping stock markets in positive territory.

- In the fixed income component, we reduced our holdings of U.S. and Canadian index-linked bonds—for which expected returns and credit spreads were too low—and instead invested in the equity markets.

We continue to favour stocks in developed countries and focus on risk management.

To learn how our funds performed:

Senior Manager, Asset Allocation and Alternative Strategies

Data source : Bloomberg

The opinions expressed here and on the next page do not necessarily represent the views of Professionals’ Financial. The information contained herein has been obtained from sources deemed reliable, but we do not guarantee the accuracy of this information, and it may be incomplete. The opinions expressed are based upon our analysis and interpretation of this information and are not to be construed as a recommendation. Please consult your Wealth Management Advisor.