Investments are very important to your financial health because they are the cornerstone of your retirement and other life projects. Registered savings plans can offer you tax benefits, such as enable you to defer income (as in the case of a RRSP) until your retirement years.

When well integrated in your financial plan, they can help grow your wealth.

TFSA

The TFSA allows Canadian residents aged 18 and older to earn investment income tax-free.

- Contributions to your TFSA are not tax deductible.

- However, all earnings accumulated in the account or withdrawn from it are not taxable, federally or provincially.

- The TFSA contribution limit for 2026 is $7,000 and will be indexed to inflation in $500 increments.

- Withdrawn amounts and unused contribution room in a given year can be carried forward to the next year.

- For an eligible individual who has never contributed to a TFSA since its creation in 2009, the current maximum contribution room would be $109,000.

- You can give money to your spouse for contributions to his or her TFSA without the attribution rules applying.

- In addition, a TFSA can generally contain similar types of investments to those in an RRSP.

RRSP and LIRA

A registered retirement savings plan (RRSP) is a plan you invest in to build up a nest egg for retirement. The main advantages of investing in a RRSP are as follows:

- The amounts you invest in the plan entitle you to a tax deduction.

- The income generated by your investments is tax-sheltered, which means your capital grows tax-free as long as the money remains in the RRSP.

- The sums invested can be used as the down payment for the purchase of your first admissible property (HBP) and for going back to school (LLP).

- Any amounts you invest and the resulting investment income are taxed only upon their withdrawal from the plan, which means that taxation is deferred until later years.

- You will realize tax savings, since it is more likely that your tax rate at retirement will be lower than your present level of taxation.

Your RRSP contributions can be invested in different investment vehicles such as deposit certificates, stocks, bonds, or mutual funds. Your Advisor can help you choose the investment vehicles best suited to your investor profile.

How much can I contribute to a RRSP?

The maximum amount you can contribute in a given year is your RRSP contribution room, which is indicated on the previous year’s federal Notice of Assessment. Each year, you can contribute up to 18% of your earned income of the previous year. Earned income includes employment income as well as net professional, business and real estate rental income. The annual contribution is subject to the following limits:

| Year | Maximum contribution |

|---|---|

| 2023 | $30,780 |

| 2024 | $31,560 |

| 2025 | $32,490 |

If you participate in an employer pension plan, your RRSP contribution room will be reduced by the annual pension adjustment (PA), which is calculated by your employer according to the terms of the pension plan. A past service pension adjustment (PSPA) can also reduce your contribution room if you buy back years of service during which you were an employee but did not contribute to the plan. If you leave the plan, the amount of your contribution room may be increased by the pension adjustment reversal (PAR) amount.

If you do not make the maximum contribution to your RRSP in a given year, the unused contribution room will be carried forward to a subsequent year.

The best way to maximize your retirement savings is to start investing early and set up a personalized strategy with your advisor.

Why contribute to your spouse's RRSP?

Contributing to the RRSP of your spouse (married or common-law) enables you to realize tax savings by splitting your income at retirement. When two spouses have different incomes or expect to have unequal incomes at retirement, contributing to the RRSP of the spouse who will have the lower income at retirement is recommended.

Income splitting

The contributions you make to your spouse’s RRSP are calculated using your own contribution room and are deductible from your income, as the “contributor.” When withdrawals are made from your spousal RRSP, your spouse will pay the applicable taxes according to his or her tax rate. Since the RRSP income will be split between you and your spouse, your respective tax rates will be lower.

Three-year rule

In order to take advantage of income splitting, your contributions to your spouse’s RRSP must remain in the RRSP for at least three years, otherwise the withdrawal becomes taxable in your hands. However, this rule does not apply when the withdrawal is made as a minimum registered retirement income fund (RRIF) withdrawal.

RRSP ownership

When a spousal RRSP is set up, both the amounts invested in it and the generated income belong to the spouse; the contributor no longer has any rights to this RRSP. However, the sums accumulated in RRSPs during a marriage constitute part of the family patrimony (if applicable) and, in the event of marital breakdown, must be taken into account when this patrimony is split. The rules pertaining to family patrimony do not apply to common-law spouses.

What happens if you contribute more than the eligible amount?

You can contribute up to $2,000 in excess of the maximum amount allowed under your RRSP without being penalized. This leeway is granted only once in a lifetime. Although this excess contribution cannot be deducted from your income, it benefits from tax-sheltered growth. If you contribute more than the allowable excess amount of $2,000 to your RRSP, you will pay a 1% penalty per month, as long as this excess amount remains in your RRSP.

Until what age can you contribute to a RRSP?

You can contribute to a RRSP up to the end of the calendar year in which you reach age 71. If you contribute to your spouse’s RRSP, your spouse must be 71 years of age or less on December 31st of the year for which the contributions are made.

Your RRSP must be converted into a RRIF no later than December 31st of the year in which you reach age 71.

Withdrawal in cash

Although it is possible to withdraw funds from your RRSP, this option is usually not recommended, as the amount withdrawn will be added to your taxable income and is also subject to tax withholdings. Depending on the situation and reason for the withdrawal, it is preferable to talk with your advisor to see which options are available to you.

Our advice

Contribute early

Start contributing at the beginning of your career, because your investments will grow tax-sheltered for longer. The table below illustrates how contributions made earlier but over a shorter period can yield more retirement capital:

| Annual year-end contribution | Total contributions | Amount accumulated in the RRSP at age 65 (annual return of 6%) |

|---|---|---|

| $2,000, age 20 to 34 | $30,000 | $283,413 |

| $10,000, age 20 to 34 | $150,000 | $1,417,064 |

| $2,000, age 35 to 64 | $60,000 | $167,603 |

| $10,000, age 35 to 64 | $300,000 | $838,017 |

Contribute early in the year…

If you prefer making annual lump-sum RRSP contributions, it is better to do so in the beginning of the year.

| Annual early-year contribution | Amount accumulated in the RRSP after 30 years (annual return of 6%) |

|---|---|

| $10,000 during 30 years | $838,017 |

| $10,000 during 30 years | $790,582 |

| Difference | $47,435 |

… or make periodic contributions

Periodic contributions level out the average cost of the investments you hold in your RRSP, which reduces the risk of investing at the wrong time. What’s more, this strategy makes it easier to manage your budget.

Contribute to your spouse’s RRSP

If you and your spouse have different incomes, consider investing in a spousal RRSP. This will enable you to balance your incomes at retirement and reduce your overall tax bill.

And if a RRSP is not enough?

Depending on the scale and extent of your needs, a RRSP may not suffice to generate the capital you will need for retirement. If this is the case, you will need to invest not only in a RRSP but also in other investment vehicles.

Your Advisor will help you determine the type of investments required to meet your retirement goals. Your Advisor can also help you achieve optimal allocation of your registered and non-registered assets.

This plan will be carried out in line with your personal retirement goals and your investor profile, with a view to benefiting from investment tax rules.

What is a LIRA?

A Locked-in retirement account (LIRA) is an account to which you can transfer “locked-in” funds from an employer pension plan, subject to a provincial law, certain annuity contracts or another locked-in retirement account. Except under certain circumstances, you cannot make any withdrawals from a LIRA, the purpose of which is to provide a life income at retirement.

What is a locked-in RRSP?

A locked-in RRSP is used when funds are transferred from an employer pension plan that falls under federal rather than provincial jurisdiction. RRSP- or LIRA-eligible investments are also eligible for a locked-in RRSP.

How do you withdraw funds from a LIRA or a locked-in RRSP?

At retirement, or earlier if you wish, funds accumulated in a LIRA can be transferred to a life income fund (LIF) or can be used to buy a life annuity. As with an RRSP, this change must be made no later than the end of the year in which you reach age 71.

Note that there is no minimum age requirement for converting a LIRA into a LIF, which means you can withdraw a portion of your locked-in funds before you reach retirement age.

Withdrawal in cash

It’s important to note that it is more difficult to withdraw from a LIRA or locked-in RRSP, as these plans fall under different laws and conditions. Therefore, withdrawals can only be done in very specific situations.

FHSA

The FHSA is a savings product for Canadian residents aged 18 and over that enables them to make contributions to a tax-free registered account with a view to buying a first home.

- The maximum annual contribution to the account is $8,000.

- The maximum lifetime contribution is $40,000.

- It is possible to carry forward up to $8,000 of unused contribution room to the next year

- Contributions made to the account are tax-deductible.

- Capital gains and interest earned in the account are non-taxable.

- Withdrawals for the purchase of a first qualifying home are also tax-free (under certain conditions) and do not have to be paid back into the account.

- The HBP and the FHSA can be used together for the down payment on a first home.

- The FHSA can remain open for a period of 15 years and must be closed either at the end of the 15th year or the year following the withdrawal for the purchase of a qualifying home.

- If not used, the amounts accumulated in the FHSA can be transferred to an RRSP when the account is closed.

If you plan to buy a home or condo, talk to your advisor. Together, you can see if the FHSA fits into your purchase plan.

For more information about FHSA, click here

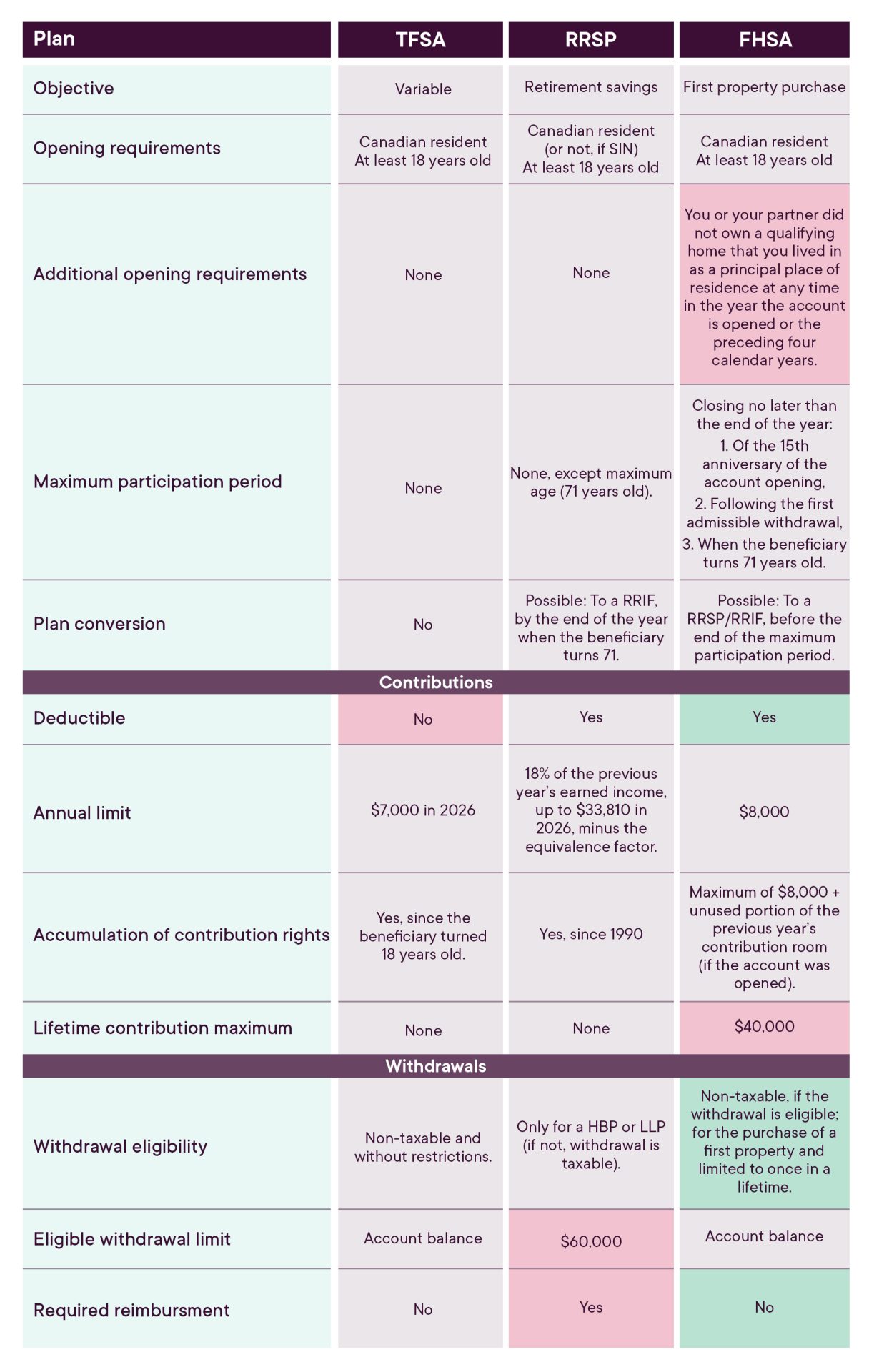

Comparing the plans

TFSA, RRSP, FHSA: what distinguishes them? They’re all registered savings plans, but each has a specific purpose, contribution terms, tax deduction potential or not… To learn more about their features, consult our comparative table!

RRIF and LIF

Retirement is a long-awaited moment for several professionals. At this stage in life, you will have to rely on several sources of income including government programs and registered savings plans, if applicable.

You must convert your RRSP/LIRA into a RIF/LIF by the end of the calendar year when you turn 71. You will also have to start withdrawing funds accumulated in your RRIF or your LIF no later than the end of the year in which you reach age 72. Otherwise, you will have to add the total value of these funds to your income for the year following the year of your 71st birthday and pay the applicable taxes.

RIFF Minimum Withdrawal Chart

| Age of the RRIF annuitant or spouse (years) | RRIF (%) | Age of the RRIF annuitant or spouse (years) | RRIF (%) | Age of the RRIF annuitant or spouse (years) | RRIF (%) |

|---|---|---|---|---|---|

| Less 71 | 1 / (90 – years) | 79 | 6.58 | 88 | 10.21 |

| 71 | 5.28 | 80 | 6.82 | 89 | 10.99 |

| 72 | 5.40 | 81 | 7.09 | 90 | 11.92 |

| 73 | 5.53 | 82 | 7.38 | 91 | 13.06 |

| 74 | 5.67 | 83 | 7.71 | 92 | 14.49 |

| 75 | 5.82 | 84 | 8.08 | 93 | 16.34 |

| 76 | 5.98 | 85 | 8.51 | 94 | 18.79 |

| 77 | 6.17 | 86 | 8.99 | 95 and over | 20.00 |

| 78 | 6.36 | 87 | 9.55 |

Source Deduction Table

| Withdrawal amount | Federal Income Tax | Québec Income Tax |

|---|---|---|

| $5,000 and under | 5 % | 15 % |

| $5,001 to $15,000 | 10 % | 15 % |

| $15,001 and above | 15 % | 15 % |

Talk to an Advisor to learn more.

Registered retirement income fund (RRIF)

A RRIF is an arrangement between you and a carrier (insurance company, trust company or bank) that is registered. You transfer the funds accumulated in your RRSP to the carrier and the carrier makes payments to you. The funds kept in a RRIF are tax-sheltered, but you are required to make minimum withdrawals each year.

These minimum withdrawals must begin no later than December 31 of the year following the establishment of the RRIF and are calculated on the basis of your age (or your spouse’s age) at the beginning of the year and the balance of the RRIF on December 31 of the previous year. There is no limit to the number of withdrawals you can make.

While minimum withdrawals are not subject to source deductions, any withdrawals above the minimum are. All amounts withdrawn from your RRIF, including minimum withdrawals, must be added to your income for the year in which you receive them.

Your age or your spouse’s?

You can choose either your age or your spouse’s to calculate your minimum RRIF withdrawals. You can always withdraw more than the required minimum from your RRIF, but if you wish to lower the amount of your minimum withdrawals, we recommend that you use the younger spouse’s age. As of age 65, you are entitled to a pension income tax credit on the first $2,000 withdrawn annually from a RRIF.

Life income fund (LIF)

A LIF is a registered account in which you transfer the sums accumulated in your LIRA.

As of January 1, 2025, major changes have been made to Quebec LIFS.

- The LIF withdrawal limit has been completely removed for persons age 55 and over to give you greater flexibility when it comes to withdrawing funds during retirement. It should however be noted that accelerating your LIF withdrawals could have an impact on certain aspects of your financial planning (partition of the family patrimony, estate plan, creditor protection).

- LIF funds cannot be transferred directly to an RRSP, RRIF or non-locked-in VRSP account.

- New rules for calculating life income and temporary income from LIFs are now in effect for persons under age 55.

Visit Retraite Québec’s website for more information.

The rules for a locked-in pension plan under federal jurisdiction are different.

- The minimal withdrawal each year is calculated in the same way as for a RRIF. However, you cannot withdraw more than the authorized maximum amount.

- The maximum withdrawal is determined each year according to different criteria (age, LIF balance, reference rate).

Annuity certain

An annuity certain is an amount you receive periodically for a pre-determined period in exchange for your capital. The amount paid depends on your capital, the period you select and the prevailing interest rates at the time of the annuity purchase.

The amounts you receive periodically are taxable in the calendar year in which they are paid to you.

Life annuity

A life annuity is an amount paid to you periodically throughout your lifetime in exchange for your capital. It may include various features, such as a guarantee, reversibility to your spouse in case of death, indexing of the amounts paid, or integration of the amounts paid with public plans.

The amount paid to you depends on your capital, your age, your sex, the features of your annuity, the prevailing interest rates at the time of the annuity purchase, and the age and sex of your spouse (if the annuity is reversible to your spouse). A life annuity purchased with locked-in funds from a retirement plan must generally be 60% or more reversible to your spouse, unless he or she signs a written waiver to the contrary.

The amounts you receive periodically are taxable in the calendar year in which they are paid to you.

RESP

A Registered Education Savings Plan (RESP) is an investment vehicle that allows you to accumulate funds to help pay for your children’s or grandchildren’s post-secondary education. Although the savings you put into the plan are not deductible from your income, the investment income they generate is not taxable until the funds are withdrawn from the account in the name of the beneficiaries.

One of the main advantages of a RESP is that it is eligible for a Canada Education Savings Grant (CESG) provided by the federal government to supplement your contributions, and the Quebec Education Saving Incentive.

Annual contribution

There is no annual contribution limit per child. Contributions can be spread over a 31-year period and may not exceed a total of $50,000 per child. Your Advisor will help you determine the amount you need to save each year according to your situation.

Canada education savings grant (CESG)

Intended for children age 17 and under, the CESG is a federal grant equal to 20% of the funds invested in a RESP account. The maximum annual grant is $500 per child, or 20% of the first $2,500 in contributions made. The maximum total grant over the life of a RESP is $7,200 per child.

If not fully used in a given year, the grant can be carried forward to a subsequent year. However, the total grant for a year may not exceed $1,000. As of 1998, grant room accumulates for a child until the end of the year in which the child turns 17.

For children age 16 and 17, the grant is paid only if at least $2,000 was invested in their RESP before they turned 16, or if at least $100 per year was invested in their RESP for four years prior to that birthday.

Québec education savings incentive (QESI)

This tax measure consists of a refundable tax credit that can be added to the RESP. One person cannot be granted more than $3,600 in total for all of the RESPs of which he/she is a beneficiary.

Educational assistance payment (EAP)

The Educational Assistance Payment is an amount paid to a student from the student’s RESP to enable him or her to pursue post-secondary studies. The EAP comes from investment income and the CESG money accumulated in the RESP. It is taxable in the hands of the student beneficiary. The total EAP payable to a full-time student may not exceed $8,000 for the first 13 weeks of an eligible education program and $4,000 for each 13-week period of an eligible part-time education program for the registered beneficiaries. There are no subsequent limits. The principal invested in the plan is returned to you tax-free.

What if the beneficiary does not pursue post-secondary studies?

The best option would be to transfer the RESP to another beneficiary, if applicable. It is important to note that the maximum amounts of grants for an individual plan still apply, and any overage must be returned to the government.

If there is no additional beneficiary or the maximum grants have been received, the grant money received must be repaid to the government, whereupon the invested contributions will be returned to you. The income accumulated in the RESP can also be returned to you in the form of accumulated income payments (AIP). These payments must be added to your income and are therefore taxable, in addition to being subject to a 20% penalty (federal: 12%; provincial: 8%).

You also have a third option: you can transfer the accumulated income payments to your RRSP or that of your spouse, provided your RRSP contribution room allows you to do so. This transfer is not subject to a withholding tax and eliminates the 20% penalty. However, it may not exceed $50,000.

To exercise either of these options, the RESP must have been in place for at least 10 years and each beneficiary must be at least 21 years of age and ineligible for an Educational Assistance Payment.

You can also, under certain conditions, name a new beneficiary or pay income accumulated in the RESP to any Canadian post-secondary educational institution.

Comparison: individual vs. family RESP

| INDIVIDUAL | FAMILY | |

|---|---|---|

| DURATION | 35 years | 35 years |

| Contributions | Until 31 years after the opening of the plan; subject to the maximum ($50,000 or more in some cases) per beneficiary. | Until the beneficiary reaches 31 years of age; subject to the maximum ($50,000 or more in some cases) per beneficiary. However, no contributions may be made for beneficiaries who are 31 years of age or older. |

| Transfer of contributions | May be transferred to any beneficiary of another plan. When the new beneficiary is the brother or sister and is under age 21, the total contributions may exceed $50,000 per beneficiary. Otherwise, the over-contribution must be withdrawn. | May be transferred to the other beneficiaries of the family plan. When the new beneficiary is the brother or sister and is under age 21, the total contributions may exceed $50,000 per beneficiary. Otherwise, the over-contribution must be withdrawn. |

| Subscribers | Anyone, even the beneficiary. | Only a parent or grandparent. |

| Beneficiaries | Only one beneficiary; can be anyone, regardless of age. | Many possible beneficiaries; they must be related by blood or adoption to each of the living subscribers or to the deceased initial subscriber and they must be under age 21 when they are named beneficiaries. |

| Grant1 | May be transferred to any plan without exceeding the lifetime limit of $7,200 per beneficiary ($3,600 for the QESI). The additional grant must be repaid if the replacement beneficiary is neither the brother nor the sister of the initial beneficiary. The Canada Learning Bond must always be repaid. | May be transferred to the other beneficiaries of the family plan who are under the age of 21, without exceeding the lifetime limit of $7,200 per beneficiary. The additional grant must be repaid if the replacement beneficiary is neither the brother nor the sister of the initial beneficiary. The Canada Learning Bond must always be repaid. |

| Advantages | The contribution period is longer than for family plans. | Grants and income can be shared between beneficiaries without having to change the beneficiary. |

| Disadvantages | Less flexible than a family plan for the payment of income and grants when the subscriber has more than one child. | The duration of the plan is limited to 35 years, which can be a significant problem if there is a big age difference between the beneficiaries. |

1Low- and middle-income families are eligible for an additional grant, based on income levels for the current year

Since 2007, the Quebec grants has been available to children under the age of 18. The maximum annual grant is $250 and corresponds to 50% of the CESG, or 10% of a $2500 contribution. Low- and middle-income families are eligible for an additional grants.

Update: 2026-01-05

Group RRSP

Employers, be prepared!

If you are an employer—regardless of whether or not you have incorporated your practice—and have five or more employees, you are directly affected by the Act respecting voluntary retirement savings plans (VRSPs). because you have to offer your employees a retirement savings plan.

Your best alternative? A customized fdp Private Wealth Management group RRSP. It’s easy to manage, it complies with requirements of the Act and is one of the most competitive products on the market!

| GROUP RRSP: EASY TO USE | Features | VRSP | ||

| Employer | Employee | Employer | Employee | |

| Employer contributions are a taxable benefit for participants and are subject to payroll taxes (EI, QPIP); they increase the QPP pension and benefits (EI, QPIP). | Increase in pension and benefits | Employer contributions have no effect on the taxable income of participants, so no increase in QPP pension or benefits (EI, QPIP) for employees. | ||

| n/a | Possible to contribute to the spouse’s RRSP | Spousal RRSP | n/a | Cannot contribute to spouse’s RRSP |

| Contributions are not locked in: they can be withdrawn at any time. | Locking-in of contributions | Contributions are locked in: they can be withdrawn according to certain conditions. | Contributions are not locked in: they can be withdrawn according to certain conditions. | |

| Accumulated amounts can be used. | Use for HBP / LLP |

Amounts accumulated by the employee can be used indirectly. | ||

| Possible at any time. | Transfer to another RRSP | Transfer to a LIRA or a LIF. | When employment ends, transfer to a RRSP, RRIF or another VRSP. | |

| May be converted to a RRIF (no later than age 71―minimum withdrawal applies), or may be used to purchase a life annuity. | At retirement | Transfer to a LIF is subject to minimum and maximum withdrawal rules, or may be used to purchase a life annuity. | May be converted to a RRIF (no later than age 71―minimum withdrawal applies), or may be used to purchase a life annuity. | |

| All fdp Private Wealth Management Series A funds. | Investment options | A default option. Otherwise, two to five other options are available. | ||

Contact an Advisor for more details and to start implementing your RRSP.

Key benefits for the employer

The group RRSP from fdp Private Wealth Management is easy to set up and flexible, which minimizes your administrative tasks.

- No administration fees or management fees for your company.

- Managing contributions is simple.

- No obligation to contribute to the plan.

- Your gateway is your advisor, who knows you well, can give you all the necessary information, and will assist you at each stage of the process.

Key benefits for the employees

Easily accessible, the advisor assigned to your company can provide your employees with all the advisory services they need for their investments.

- Each employee retains ownership of their RRSP and has access to programs like the HBP or the LLP.

- Employees can obtain an immediate tax reduction, since contributions are deducted from their gross salary.

- According to their investor profile, they can customize their portfolio using a variety of Professionals’ Financial mutual funds.

- They have direct access to their RRSP account at all times via the fdp Private Wealth Management website.

IPP

An Individual Pension Plan is a defined contribution registered pension plan that enables companies to save for the retirement of an important employee or a key shareholder.