Yann Furic

B.B.A., M. Sc., CFA®

Senior Portfolio Manager, Asset Allocation and Alternative Strategies

In 2025, several international markets, including Canada, Europe and Japan, as well as the emerging market index, outperformed the S&P 500.

Investors drawn to global stock markets outside the United States

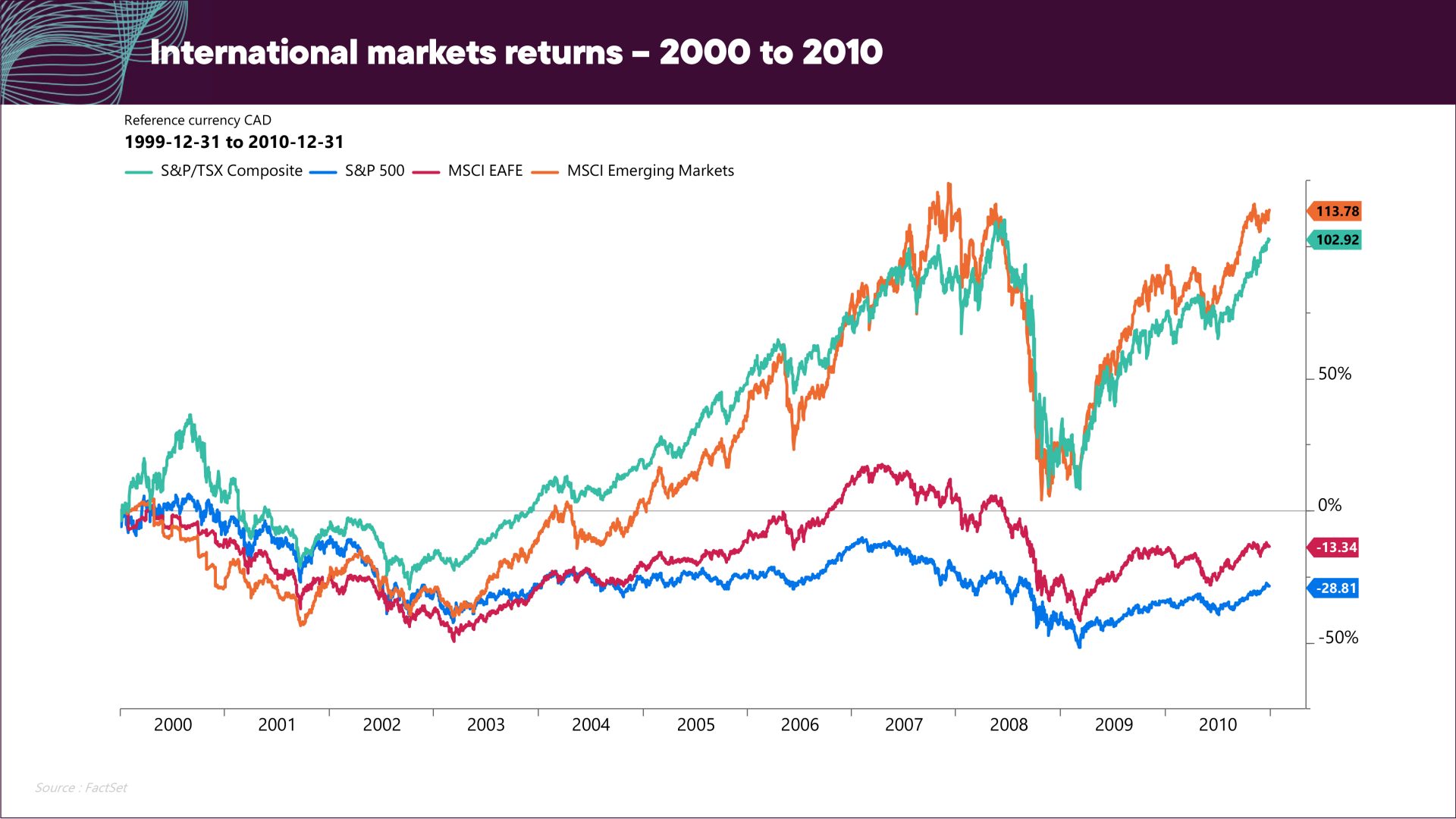

This trend could well continue in 2026, and it’s worth noting that during the period from 2000 to 2010, the Canadian, emerging economies, and EAFE stock markets all outperformed the S&P 500.

In recent months, there has been a strong trend toward limiting exposure to U.S. large-cap technology stocks and diversifying investments.

This does not mean that investors have sold off their U.S. stocks en masse, but rather that they are looking to invest differently and diversify their portfolios. The popularity of the theme of massive infrastructure construction for the deployment of artificial intelligence (known as “AI server farms”) has now given way to questions about the profitability of these investments. In other words, investors will want to assess the profits that will be generated by these considerable expenditures. For example: how many users will there be for Copilot, Microsoft’s virtual assistant, and how much will they be willing to pay monthly for this service?

The global economy continues to grow, and government measures or initiatives such as increased defence spending in Europe and fiscal stimulus in Japan following the recent elections are positive factors for stocks considered cyclical.

What do we mean when we talk about “cyclical” stocks? These are usually stocks in the financial, industrial, materials, and energy sectors. They are called “cyclical” because their profitability is linked to the economic cycle, as opposed to non-cyclical stocks such as those in the healthcare or consumer staples sectors, for example.

These sectors carry more weight in countries outside the United States. Non-cyclicals represent nearly 80% of the S&P/TSX index, 54% of EAFE markets, and 41% of emerging markets, but only 27% of the S&P 500.

In addition, a weaker U.S. dollar has historically been positive for emerging markets.

The small-cap segment is also making a comeback. In the U.S., deregulation efforts in many industries and a lower impact of tariffs are positive factors. Elsewhere, such as in Europe and Japan, higher government spending should boost small caps, which are strongly impacted by more local situations and events.

Higher returns outside the U.S. were the norm in the early 2000s, and we could see a repeat of this.

Canadian and U.S. policy rates: next meetings on March 18, 2026

On Wednesday, January 28, the Bank of Canada (BoC) decided to leave its target rate unchanged at 2.25%. This decision was anticipated by the market, as the release of employment data on Friday, January 9, showed job creation rather than job losses. Markets are anticipating a possible rate cut in December 2026.

South of the border, a new chair has been appointed to the U.S. Federal Reserve (Fed). Kevin Warsh, who previously served as a Fed governor from 2006 to 2011, will take office in May 2026, succeeding current chair Jerome Powell. His appointment was well received by the markets. He is expected to promote the idea that productivity gains associated with the deployment of artificial intelligence should enable economic growth without inflation, and therefore a reduction in key interest rates. It should be noted that the Fed’s decisions are taken by a majority of the 12 persons who make up the FOMC (Federal Open Market Committee), which meets eight times a year to discuss monetary policy and decide on key interest rates. As for possible rate cuts in 2026, the markets are anticipating two or three.

With regard to key interest rates, the central banks of Europe, Japan, and Canada are on hold or even considering increases, especially in Japan and Australia, which has already raised rates. If such divergences in global monetary policy continue to widen, they are likely to weaken the U.S. dollar.

One of the surprises of 2025 was in fact the weakness of the greenback, especially against the euro. The pressure exerted by the U.S. president on the Fed to lower its key interest rates, combined with the imposition of tariffs, meant that inflation remained higher than expected, which reduced the value of the U.S. dollar and its purchasing power, drove up the price of gold, and made exports less expensive for the U.S. administration.

Employment rebound in Canada

The loss of 24,800 jobs in January fell well short of expectations, which called for the addition of 5,000 jobs. It was mainly full-time jobs (+45,000) that boosted the labour market, while the sharp decline in workers in January was due to the loss of part-time jobs (-70,000). Since the labour force declined, the unemployment rate fell to 6.5%, while wage growth remained strong at 3.3%.

Tariffs: still awaiting a Supreme Court decision

During the November 5 hearing on the legality of tariffs imposed by the U.S. administration on many countries, the justices of the U.S. Supreme Court appeared skeptical of the government’s arguments. A ruling will be issued by next summer, but the markets are expecting a decision much sooner.

It should be noted, however, that the market reaction could be weaker than anticipated a few months ago. Markets react to what differs from the consensus. Currently, investors expect the decision to prevent the use of tariffs in part or in full.

However, there is one unknown factor that could still cause market volatility: will the Court order the reimbursement of tariffs already collected?

A decision against the U.S. administration would not necessarily mean the abolition of all tariffs, but it would require a different legal process for imposing them, which would limit the power of government authorities to impose tariffs at will.

OVERVIEW OF GLOBAL EQUITY MARKETSAll percentages are in Canadian dollars. |

||||

|

Country |

Index |

Return |

Change |

Year-to-date return in 2026 |

|

Canada |

S&P/TSX |

0.84% |

|

0.84% |

|

United States |

S&P 500 |

0.22% |

|

0.22% |

|

|

Nasdaq |

-0.26% |

|

-.0.26% |

|

International stock markets |

EAFE |

3.94% |

|

3.94% |

|

Emerging markets |

|

7.53% |

|

7.53% |

|

China |

MSCI China |

3.43% |

|

3.43% |

The return shown is the total return, which includes the reinvestment of income and capital gains distributions

Source : Morningstar Direct.

RETURN ON CANADIAN BONDS |

|

| Index | Return from January 1 to 31, 2026 |

| FTSE Canada Universe Bond Index | 0.58% |

Source : Morningstar Direct

Data influencing the markets

CANADA |

UNITED STATES |

Recession Indicator |

|

Moderate |

Moderate |

Policy Rates |

|

2.25% |

3.50% – 3.75% |

|

No change was announced on January 28, 2026. No cut is planned for 2026. According to the BoC, GDP growth is expected to remain positive in 2026. |

The U.S. Federal Reserve kept its key interest rates unchanged on January 28, 2026. Uncertainty surrounding inflation and employment persists. Possibility of two or three rate cuts in 2026, but nothing is certain. |

Employment Situation |

|

|

Jobs added: 24,800 Expectations: addition of 5000 |

Jobs added: 130,000 Expectations: addition of 55,000 |

|

Wage growth: 3.3% Expectations: 3.7% |

Wage growth: 3.7% Expectations: 3.6% |

|

Unemployment rate: 6.5% Increase: 0.3% |

Unemployment rate: 4.3% Decrease: 0.1% |

| Most jobs lost were part time. |

|

Inflation |

|

|

January: 2.3% Change: -0.1% |

January: 2.4% Change: -0.3% |

Overall, what are the economic indicators telling us?

Benchmark rates (Canada, Europe and the United States) ![]()

- The Federal Reserve kept its rates unchanged in January. A new chair has been appointed and will take office in the coming months. The market is forecasting two or three further rate cuts in 2026. In Canada, no cuts are expected over the next year.

- Europe is on hold and will react to future economic data. Inflation is lower there and the real impact of tariffs is yet to come.

- The U.S. Supreme Court’s ruling on tariffs could have an impact on inflation, economic growth, and monetary policies around the world.

Global Purchasing Managers’ Index ![]()

- Manufacturing segment: positive, with more than half of the 30 countries in this segment posting a reading above 50 (expansion).

- Services segment: continues to hold steady and remains robust.

Inflation rate ![]()

- Overall: stable, but fears of an upsurge are emerging.

Factors to watch

- Deregulation in various industries in the United States: this should help maintain economic growth and encourage investment. Other countries, such as Canada, will have to follow suit or risk losing competitiveness.

- Introduction of populist policies in the United States: these could undermine deregulation efforts. Limiting credit card interest rates, preventing institutional investors from owning homes, and allowing government entities to purchase mortgage products could create distortions and reduce economic growth.

- Trade tensions: supported by the indiscriminate use of tariffs, they could cause an economic slowdown and increase inflation. This situation could lead to an episode of stagflation, the most negative economic scenario. The trade agreement between Canada, Mexico, and the United States will have to be renegotiated in 2026.

- Inflationary scenarios: if they result in keeping yields on five-to-ten-year maturities at high levels, they should be avoided at all costs, as they would slow business investment and the reshoring of production lines to the United States.

- Geopolitical uncertainty: Tension between the United States and Iran, the Russia-Ukraine war, regional conflicts in the Middle East, tensions between the U.S. and China, possible annexation of Taiwan by the Chinese government, return of the Monroe Doctrine in the United States.

fdp tactical views – January 2026

- We maintained the equity weighting in the tactical allocation strategy.

- Economies continue to grow. Large companies are generally reporting solid earnings, which is keeping stock markets in positive territory.

- We maintained our weighting in U.S. equities.

- We kept our positioning in Europe and our overweight in Japan.

- We maintained the weight of emerging market equities and increased the weight of quality U.S. small caps. Lower interest rates in the United States, new quantitative easing measures, and a stable economy all argue in favour of a position in small caps.

- In the fixed income component, we maintained the weighting of high-yield bonds and foreign bonds. We hold various types of debt through U.S. and emerging market government issues.

We continue to favour stocks in developed countries and focus on risk management.

To learn how our funds performed:

Senior Manager, Asset Allocation and Alternative Strategies

Data source : Bloomberg

The opinions expressed here and on the next page do not necessarily represent the views of Professionals’ Financial. The information contained herein has been obtained from sources deemed reliable, but we do not guarantee the accuracy of this information, and it may be incomplete. The opinions expressed are based upon our analysis and interpretation of this information and are not to be construed as a recommendation. Please consult your Wealth Management Advisor.