Yann Furic

B.B.A., M. Sc., CFA®

Senior Portfolio Manager, Asset Allocation and Alternative Strategies

Global stock markets had a generally positive June, rounding out an excellent first half of 2026.

Diversification of market returns: a positive sign

The next round of quarterly earnings reports will begin to be released during the week of July 12 and will culminate with reports from major tech companies at the end of the month.

During this earnings season, spending on artificial intelligence and the entire associated ecosystem will come under close scrutiny. There have been some fluctuations in recent weeks as investors questioned the scale of current spending on AI development. Despite these concerns, other sectors quickly took the lead, helping the markets avoid a sharp decline.

This rotation is encouraging because it shows that the market rise depends not only on technology, but also on a broader range of sources of returns.

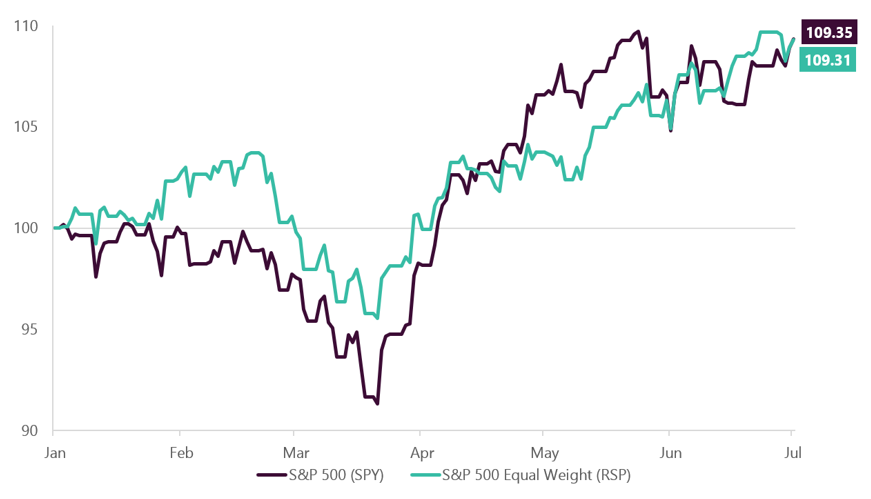

The chart below compares two ways of looking at the S&P 500 Index since the beginning of the year using two indices: the SPY U.S. Equity and the RSP U.S. Equity.

- The SPY (purple line) reflects the S&P 500 as it is typically viewed, where the biggest companies—often in the technology sector—have a greater weighting in the index and therefore exert a greater influence on the overall performance.

- The RSP (turquoise line) includes the same companies but assigns them all the same, equal weight. It shows whether the overall performance is driven by a larger number of companies or only by the biggest ones.

The fact that the two indices show very similar results (9% year-to-date) indicates that the market rise is not driven solely by a few big technology companies. Rather, it is spread across several companies and sectors, reflecting a more balanced market.

S&P 500 Returns (SPY and RSP) Year to Date in 2026

Despite the geopolitical uncertainty of recent months, corporate profits have held up and have supported the ongoing economic cycle.

Monetary policy and central banks

Last June, the new chair of the U.S. Federal Reserve (Fed), Kevin Warsh, presided over his first meeting in his new role. While some observers expected rates to remain at their current levels and for the Fed to signal a rate cut in the coming months, they instead heard remarks suggesting possible rate hikes in the near future. It should be noted that persistent inflation exceeding the target, as well as recurring increases in gasoline prices due to the U.S.–Iran conflict, continue to militate in favour of a hawkish bias in the future. An important fact to remember: the Fed’s decisions are made by consensus among a group of 12 governors, not solely by the chair.

In Europe, the European Central Bank (ECB) raised key interest rates to combat inflation.

The Bank of Canada (BoC) remains on pause and kept its rates unchanged at its July 15 meeting.

Finally, the Bank of Japan (BoJ) raised its interest rates by 0.25% to counter inflationary pressures and slow the yen’s depreciation.

Positive but fluctuating employment situation

Job creation in Canada was higher than expected, with 18,200 jobs added, mainly part-time positions. The private sector, particularly the services sector, drove this growth, while 30,500 jobs were lost in the public sector—the highest number since the pandemic began.

In the United States, job creation was positive but lower than anticipated. For several months now, the country has seen stable but weak job growth.

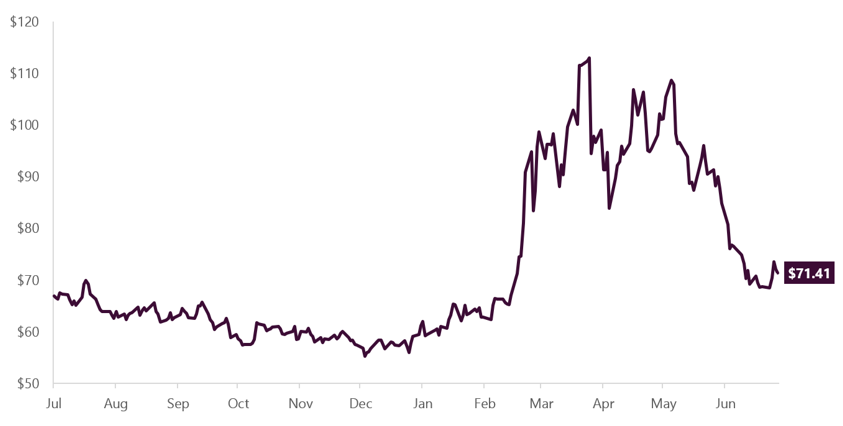

Oil prices and the U.S.–Iran conflict

This conflict continues to make daily headlines, but financial markets are now pricing in the scenario that the Strait of Hormuz will remain open. Oil prices continue to serve as a good indicator: after fluctuating between US$90 and US$110 from March through June, they now range from US$70 to US$75. Increased production in the United States, the announcement by OPEC countries that they would raise production quotas, the development of alternative supply routes, and weak demand from China are all contributing to keeping prices lower.

Year-over-Year Fluctuation in Oil Prices – July 2025 to June 2026

The future of CUSMA negotiations

Since July 1 has passed and no partner has terminated the agreement, it is understood that an annual negotiation process will be in effect for the next ten years. If no new agreement is reached during this decade, the current CUSMA will expire in 2036.

Information from the United States suggests that of the three possible scenarios:

- renewal of the agreement as is,

- withdrawal of one of the partners,

- annual renegotiation for a maximum period of ten years,

the last option will be chosen since most U.S. states want the agreement to continue.

The most negative aspect of these annual negotiations is that companies will not know what to expect from one year to the next and may put their development projects on hold.

This observation applies to all three partners.

Financial market performance last month

OVERVIEW OF GLOBAL EQUITY MARKETSAll percentages are in Canadian dollars. |

||||

|

Country |

Index |

Return* |

Change |

Year-to-date return in 2026 |

|

Canada |

S&P/TSX |

0.50% |

|

11.17% |

|

United States |

S&P 500 |

2.01% |

|

14.07% |

|

|

Nasdaq |

0.16% |

|

17.10% |

|

International stock markets |

EAFE |

3.06% |

|

13.28% |

|

Emerging markets |

|

1.54% |

|

28.18% |

|

China |

MSCI China |

-4.31% |

|

-11.99% |

*The return shown is the total return, which includes the reinvestment of income and capital gains distributions

Source : Morningstar Direct.

RETURN ON CANADIAN BONDS |

|

| Index | Return from January 1 to June 30, 2026 |

| FTSE Canada Universe Bond Index | 0.51% |

Source : Morningstar Direct

Data influencing the markets

CANADA |

UNITED STATES |

Recession Indicator |

|

Moderate |

Moderate |

Policy Rates |

|

2.25% |

3.50% – 3.75% |

|

No change was announced by the Bank of Canada on July 15, 2026. The BoC remains optimistic about GDP growth in 2026. |

The U.S. Federal Reserve kept its policy rates unchanged on June 17, 2026. Uncertainty surrounding inflation and employment persists and is compounded by inflationary pressures stemming from the conflict with Iran. |

Employment Situation |

|

|

Jobs gained: 18,200 Expectations: gain of 10,000 |

Jobs gained: 57,000 Expectations: gain of 110,000 |

|

|

|

|

Wage growth: 3.7% Expectations: 3.6% |

Wage growth: 3.5% Expectations: 3.8% |

|

Unemployment rate: 6.5% Expectations: 6.6% |

Unemployment rate: 4.2% Expectations: 4.3% |

Inflation |

|

|

June: 2.8% Change: 0.4% |

June: 3.5% Change: -0.7% |

Overall, what are the economic indicators telling us?

Benchmark rates (Canada, Europe and the United States) ![]()

- U.S. Federal Reserve (Fed): no change in rates in June. Kevin Warsh’s first press conference as the new Fed chair.

- Bank of Canada: no change in rates, with close monitoring of the consequences of the conflict in Iran. Possible rate hike over the next year.

- European Central Bank (ECB): rate hike at its last meeting and awaiting future economic data. Expectations of one or two rate hikes this year due to the conflict in Iran and its impact on energy prices.

Global Purchasing Managers’ Index ![]()

- Manufacturing segment: positive, with 25 of the 30 countries in this segment posting a reading above 50 (expansion).

- Services segment: continues to hold up.

Inflation rate ![]()

- Overall: concerns are emerging about a rise in inflation due to the conflict with Iran and energy prices. General trend: rates are expected to remain unchanged or rise.

Factors to watch

- Conflict with Iran: the global tensions it is causing, and especially the impact on traffic in the Strait of Hormuz, will have an impact on corporate earnings. The longer the conflict drags on, the greater its repercussions will be, but supply chains are increasingly adjusting.

- Deregulation in various industries in the United States: this should help maintain economic growth and encourage investment. Other countries, such as Canada, will have to follow suit or risk losing competitiveness.

- Trade tensions: supported by the indiscriminate use of tariffs, they could cause an economic slowdown and increase inflation, resulting in an episode of stagflation, the most negative economic scenario. The trade agreement between Canada, the United States and Mexico (CUSMA) is now in the annual renegotiation phase, which could create a climate of uncertainty in terms of corporate investment.

- Inflationary scenarios: if they result in keeping yields on five-to-ten-year maturities at high levels, they should be avoided at all costs, as they would slow business investment and the reshoring of production lines to the United States.

- Geopolitical uncertainty: conflict between the United States and Iran, the Russia-Ukraine war, regional conflicts in the Middle East, tensions between the U.S. and China, possible annexation of Taiwan by the Chinese government, return of the Monroe Doctrine in the United States.

fdp tactical views – June 2026

- We increased the equity weighting in the tactical allocation strategy in all geographies.

- We prefer stocks to corporate bonds, whose spreads remain historically tight.

- Economies continue to grow. Large companies are generally reporting solid earnings, which is keeping stock markets in positive territory.

- In the fixed income component, we reduced our holdings of U.S. bonds—for which expected returns and credit spreads were too low—and instead invested in the equity markets.

We continue to favour stocks in developed countries and focus on risk management.

To learn how our funds performed:

Senior Manager, Asset Allocation and Alternative Strategies

Data source : Bloomberg

The opinions expressed here and on the next page do not necessarily represent the views of Professionals’ Financial. The information contained herein has been obtained from sources deemed reliable, but we do not guarantee the accuracy of this information, and it may be incomplete. The opinions expressed are based upon our analysis and interpretation of this information and are not to be construed as a recommendation. Please consult your Wealth Management Advisor.