Let’s first take a look at the major global trends that shaped the first half of the year:

- The conflict in the Middle East and its impact on markets and inflation

- Persistent inflation, driven in part by energy prices

- The surprising resilience of financial markets, despite this uncertain environment

- The continued momentum of AI, particularly in the United States, but also elsewhere in the world

- Corporate profits that exceeded expectations and were revised upward. This earning growth:

- supported market gains, despite concerns about the economy;

- changed perceptions of valuations, because although markets seem high, earnings have grown faster than stock prices, and valuations are less excessive than expected.

Optimism, growth and uncertainty

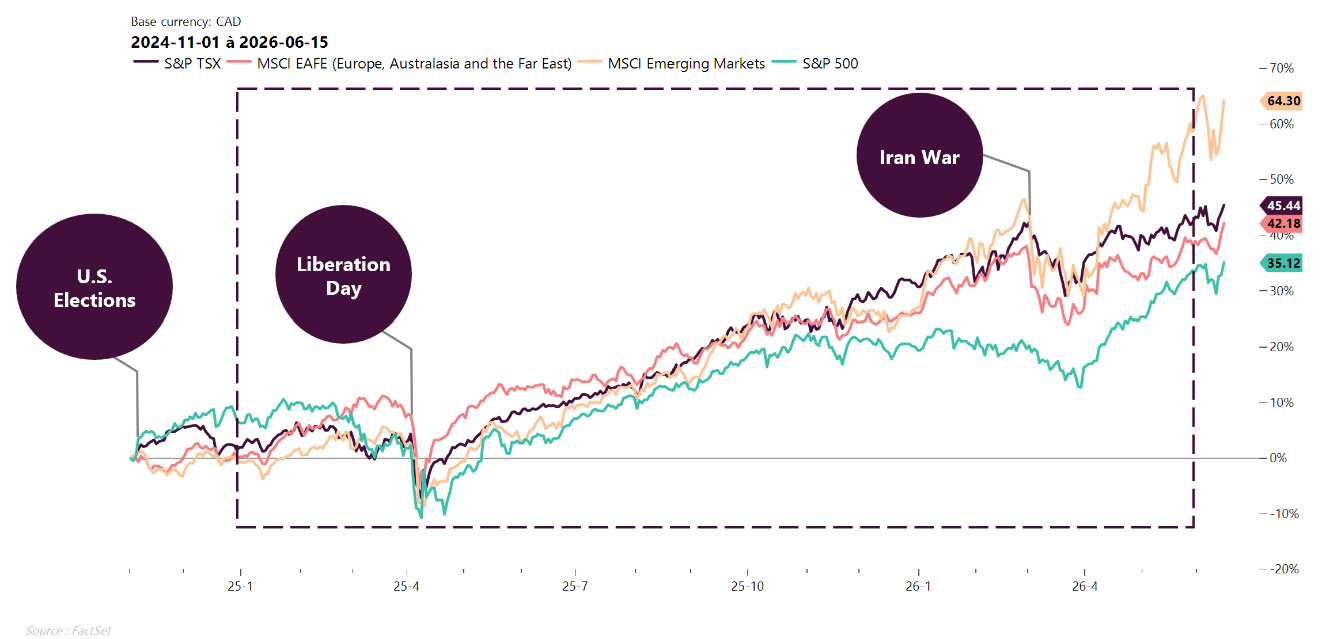

Since November 2024, stock markets have benefited from widespread optimism, U.S. growth and momentum driven by AI. In 2026, conditions became more challenging as these same markets showed uneven growth and central banks became less accommodative. Growth nevertheless continued, despite the shock caused by the Iran war.

Bond markets

A shift from a cycle of easing to an environment of prolonged stability or tightening.

Bond markets are operating in an environment where inflation remains persistent and limits central banks’ room to maneuver. Contrary to expectations at the start of the year, little or no monetary easing is anticipated in the short term. Rates could remain high for longer or even rise again if inflation persists. The expected support from central banks is therefore more limited.

Canadian bonds

Canadian bonds

- A mixed picture: the economy has weakened, but inflation is still very much with us.

- Keeping interest rates high is a measure that could be used to curb inflation, despite a sluggish economy and challenges for consumers when renewing their mortgages.

U.S. bonds

U.S. bonds

- Things to watch: changes at the Fed and statements by the new chair, Kevin Warsh.

- The economic environment remains resilient, with rates expected to stay high.

- We are seeing a potentially more restrictive trend in the short term, with yields already on the rise.

European bonds

European bonds

- For the second half of the year: likelihood of a bigger rise in yields than in other markets.

Stock markets

Key themes that drove the markets: energy (linked to the conflict with Iran), AI and corporate earnings (more affordable markets).

Canadian market – It could still offer potential for returns, albeit more moderate and uneven. Gains will come mainly from natural resources, exports and the financial sector, particularly banks. By contrast, sectors tied to household consumption are expected to grow at a slower pace, given that the domestic economy remains fragile. The market may therefore perform well, but it will remain heavily dependent on commodities and constrained by Canada’s economic weakness.

U.S. market – The outlook is more favourable than for the Canadian market. U.S. corporate earnings continue to support valuations: although markets appear expensive, rising earnings make valuations less excessive than they appear. Three factors should continue to support the U.S. market over the coming months: household consumption, which remains resilient; spending on artificial intelligence, which continues to grow and is expected to remain high and visible for the next 18 to 24 months; and government spending, with expansionary budgets contributing to growth despite high deficits.

International markets outside the U.S. – European and Japanese markets remain more sensitive to the economic cycle due to their significant exposure to cyclical sectors such as metals, energy, banking and industrials. Against the backdrop of a global economic recovery following the resolution of the conflict in the Middle East, these markets could therefore be well-positioned to benefit. Conversely, prolonged tensions could keep inflationary pressure high and curb their recovery potential.

International markets outside the U.S. – European and Japanese markets remain more sensitive to the economic cycle due to their significant exposure to cyclical sectors such as metals, energy, banking and industrials. Against the backdrop of a global economic recovery following the resolution of the conflict in the Middle East, these markets could therefore be well-positioned to benefit. Conversely, prolonged tensions could keep inflationary pressure high and curb their recovery potential.

Emerging markets – The outlook remains tied to two key drivers: global demand related to artificial intelligence and evolving trade relations between China and the United States. As is the case with our American neighbor, emerging markets could benefit from AI-related spending, particularly due to demand for components, technological infrastructure and certain Asian supply chains. A trade détente between China and the United States would also help reignite growth in China’s manufacturing sector and, by extension, global trade. In the absence of a genuine recovery, China’s role could be one of a stabilizer rather than a driver of growth.

Emerging markets – The outlook remains tied to two key drivers: global demand related to artificial intelligence and evolving trade relations between China and the United States. As is the case with our American neighbor, emerging markets could benefit from AI-related spending, particularly due to demand for components, technological infrastructure and certain Asian supply chains. A trade détente between China and the United States would also help reignite growth in China’s manufacturing sector and, by extension, global trade. In the absence of a genuine recovery, China’s role could be one of a stabilizer rather than a driver of growth.

Global trends to watch

- Ever-increasing spending on AI and its growing use across many economic sectors.

- Rising military spending due to uncertainty surrounding national security issues. This trend could support certain sectors related to defence, aerospace, infrastructure and security technologies, particularly in Canada and Europe. However, it places additional pressure on public finances, at a time when budget deficits are already high.

- Inflation and central banks: striking a balance is difficult due to potential rate hikes and their impact on the economy.

The growth potential of AI: greater selectivity

AI remains a powerful driver of growth and innovation, but the challenge is no longer simply about having exposure to it. We must now distinguish the long-term winners from the more vulnerable companies, as performance gaps could be significant. AI extends far beyond visible applications like ChatGPT to include infrastructure, semiconductors, software, cloud computing and many supply chains. This calls for a selective, diversified and tactical approach.

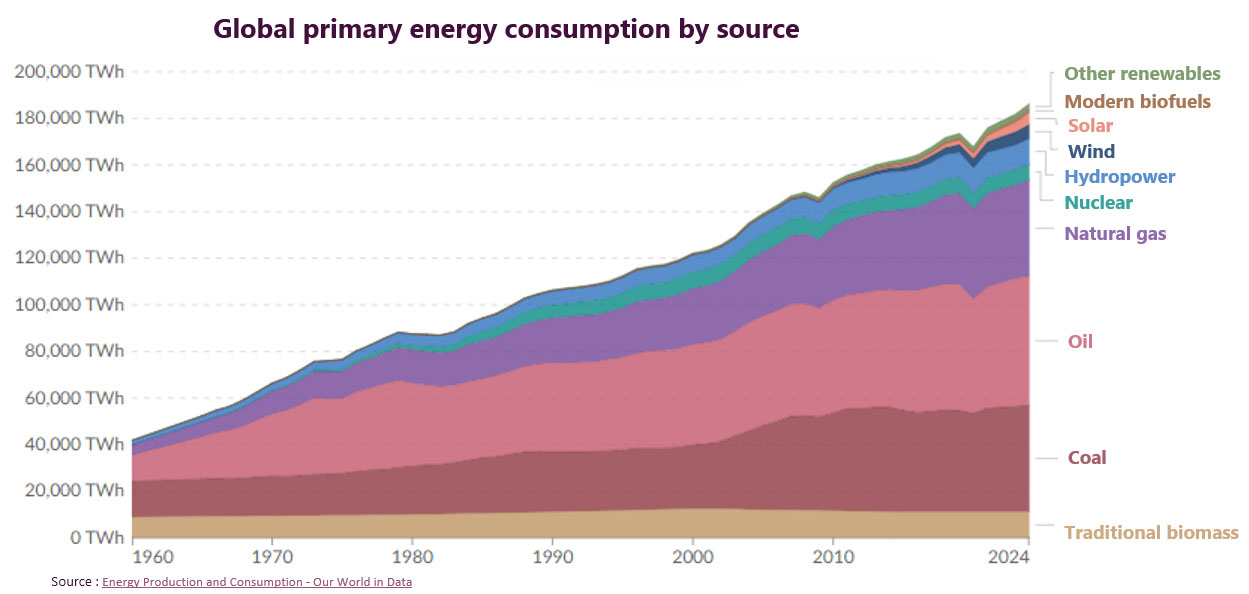

The energy issue

- We are currently experiencing an energy-intensive phase of global development, which is driving high demand across all energy sectors.

- Contrary to what was anticipated, the integration of renewable energy sources is not replacing conventional energy sources: these sources complement each other to meet the enormous global demand. While some energy sources may reach a plateau (coal), there is no letup in sight in terms of demand.

Our tactical positioning

- Maintain a focus on quality by investing in companies with healthy balance sheets and solid earnings.

- Equities: overweight with a bias towards the U.S. market and an underweight position in European and Japanese markets.

- Bonds: given the high cost of borrowing and the risk of inflation, favour shorter maturities.

Our overall investment vision

At the time of writing these lines, the second half of 2026 will likely see geopolitical or financial turbulence that could test the resilience of the markets, while also creating attractive opportunities. We are therefore keeping a close eye on how events unfold so that we can respond quickly, while keeping them in perspective within the broader context.

Although political and economic developments can cause market volatility, these fluctuations are usually temporary and markets quickly stabilize. If you have any questions or concerns, contact your advisor. You can always count on their expertise.

Daniel Solomon

M Sc., CFA

Vice-President and Chief Investment Officer

Yann Furic

B.B.A., M. Sc., CFA®

Senior Portfolio Manager, Asset Allocation and Alternative Strategies

Max D’Alessandro

CFA®

Senior Portfolio Manager, Fixed Income and Alternative Strategies