Is the rise in inflation starting to seriously worry you? It’s hard to remain indifferent to a situation that could impact your financial plan!

Since the beginning of 2022, we have witnessed surprising jumps in inflation, as evidenced by data from Statistics Canada,[1] according to which the inflation rate was 5.1% in January; it then accelerated to 5.7% in February and hit 6.7% in March. You have to go back to September 1991 to find an inflation rate of 5% in Canada! This rise is even more spectacular if we consider that just over a year ago, in January 2021, inflation was at 1%!

Sectors under pressure

That said, it should be noted that mounting inflation is hitting certain specific sectors much harder, notably energy and food, but that eventually the effect will spread, since everything is connected in the global economy.

In practical terms, pervasive inflation raises concerns, particularly when it comes to financial planning and retirement planning. The Bank of Canada and the U.S. Federal Reserve have started to raise their respective policy rates in order to slow the trend, and they will implement further rate hikes periodically through 2022. The increase in the policy rate will, however, have an effect on mortgage rates, consumer credit and business financing.

Understand the issues

To help you make sense of it all, fdp wealth management advisors have identified the issues most frequently raised by their clients.

First, your financial plan.

Does it take into account exceptional situations, such as the one we are currently experiencing?

Yannick Bernier, advisor and financial planner, comments:

« First, you should know that a long-term financial plan is developed according to the Guidelines of the Institut de planification financière du Québec (IQPF). »[2].

How does the IQPF establish the recommended inflation rate assumption?

In its publication Projection Assumption Guidelines dated April 30, 2021, the IQPF and FP Canada established the Guidelines for the year 2021. In this document, they develop the financial assumptions that a financial planner should use to make long-term financial projections (more than 10 years). They write: “Predicting the direction the economy will take and how financial markets will evolve is a difficult exercise requiring the integration of a large number of variables and highly sophisticated valuation models. To protect themselves and their clients, financial planners are encouraged to rely on these Guidelines.”[3]

What is the useful life of the Guidelines?

“The Guidelines are updated annually[4] and although some of the assumptions […] may change from time to time, this does not mean that projections based on previously published assumptions are no longer valid.”[5]

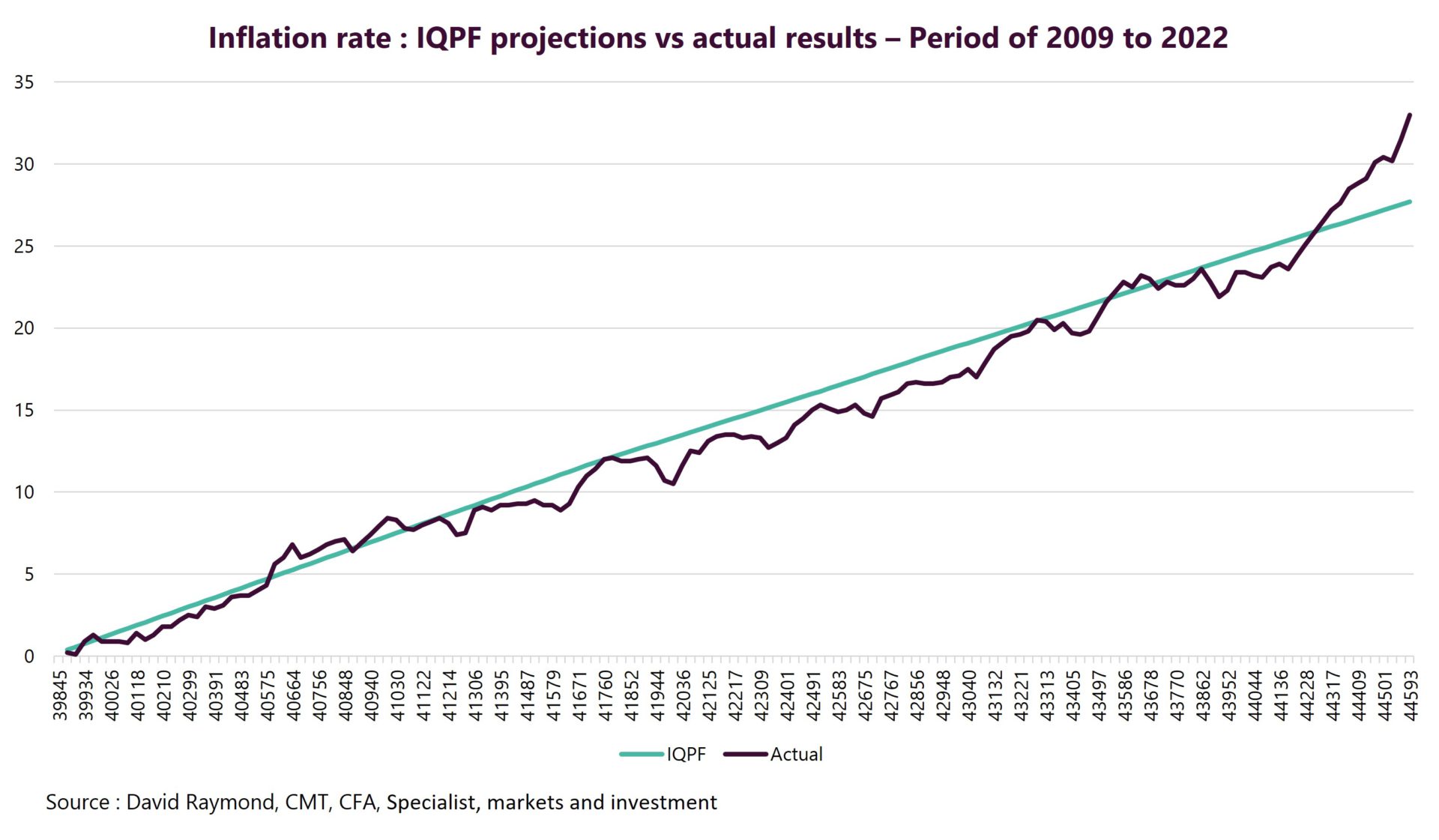

Here is a comparative table of the IQPF’s inflation projection assumptions, as well as the real inflation rate observed over a period of 13 years, i.e. from 2009 to 2022. You will note that the IQPF’s inflation projections are often higher than the actual inflation readings.

[3] https://www.iqpf.org/docs/default-source/outils/iqpf-2021-projection-assumption-guidelines.pdf (page 6)

[4] Ed. Note: April 30

[5] https://www.iqpf.org/docs/default-source/outils/iqpf-2021-projection-assumption-guidelines.pdf (page 6)

In recent years, the IQPF advised us to use 2% as the inflation rate in financial plans. For retirement, we have to take into account a net rate of return on investments that includes inflation.

- If we project a return of 4.10% and subtract 2%, that gives 2.10%.

- Assuming that inflation could persist between 3% and 4%, with a long-term return on an investment portfolio of 5% or 6%, we would obtain a similar net result of 2%.

In the 1990s, the inflation rate was above 10%, but bond yields allowed for a similar net return. Returns have exceeded expectations in recent years, when inflation was at or below 2%, especially in 2020. During this period, returns obtained by investors were significantly higher than projections.

The important thing is to have a good plan, with realistic assumptions. Some years will be better, others not so good. We cannot control inflation and even the Bank of Canada, which regulates it to some extent with its policy rate, is having difficulty influencing it and reducing it at present, because the situation is more of a global issue concerning supply chains and war.

When I make a financial plan with a client, inflation is a key consideration. I have to make them aware of the method of calculating inflation and of indexing government or private retirement pensions. I have to help my clients protect themselves from inflation and make the best decisions, such as the age at which to retire.

If your plan is done properly, spikes in inflation over short periods shouldn’t lead to major changes in your financial strategy. A good conservative retirement plan normally includes the necessary leeway to absorb the risk. That said, special circumstances may lead to certain readjustments. That is when you need to talk to your advisor to find solutions. You have to raise the question and not wait: together, we will tailor your financial plan to your reality.”

Inflation is experienced daily and can sometimes force you to reconsider certain aspects of your financial plan. What should be prioritized in your decisions?

Anie Sansoucy, advisor and financial planner, examines certain factors that could be problematic:

“The mistake to avoid is reducing the amount of your savings. Before doing that, many solutions are possible.

Do you have a variable-rate mortgage?

- Simulate a rate increase of 2 or even 3 percentage points on your mortgage payments. If the impact on your budget is such that it would force you to reduce the amount of your savings, or if it jeopardizes your ability to repay your loan, I recommend that you contact your mortgage broker in order to convert your variable-rate loan to a fixed-rate loan.

- Even though, in the long term, a variable rate is almost always more advantageous, in the short term, rate increases can generate concerns. To benefit from the advantages of a variable rate and maintain your peace of mind, I recommend that you make the same payments as if you had chosen a fixed rate. This way, in addition to repaying your principal more quickly, you give yourself some protection against rate increases.

Have you reviewed your budget recently?

- Analyze your different budget items and make sure the allocated amounts are still realistic. If you closely monitor your budget and quickly adjust your expenses, you maximize your chances of staying on track with your goals.

By maintaining control over your cash outflows, you avoid unpleasant surprises. It’s a temporary measure, until the economy stabilizes, but the exercise is really worth it.

Is your investment portfolio diversified?

- For some, owning stocks means taking risks. In reality, with an overly conservative portfolio, you run the risk that your savings will not cover inflation, which means that your purchasing power will erode over the years. A good, well-diversified portfolio of equities and fixed income will allow you to maintain your purchasing power over the long term.

- Inflation often goes hand in hand with stock market volatility: resist the temptation to exit the market, maintain your long-term view and don’t stop investing.

Do you know your retirement income?

- Do you have a pension fund? Do you know what the indexation rate of your retirement pension will be? Many pension funds have capped their annual pension indexation rate. Over a long-term horizon, this could have disastrous consequences on the financial situation of a pensioner. To ensure a comfortable retirement, having an investment portfolio will help you maintain your standard of living.

Remember that your professional and personal situation is unique and that the best way to address your concerns is to discuss them with your advisor. We’re here to help you.”

In conclusion

How long will these inflationary spikes last? It’s difficult to predict, but it seems clear that we will have to deal with this uncertainty for some time yet. This is the time to examine your financial situation calmly and to proactively take steps that will allow you to reduce your financial stress and stay on track. Don’t hesitate to contact your advisor to assess your situation and take advantage of their advice.

[1] https://www150.statcan.gc.ca/n1/daily-quotidien/220216/dq220216a-eng.htm

[2] The Institut québécois de planification financière is an organization whose mission is to protect the personal finances of the public by training financial planners and establishing standards of professional practice.