Want to know all about the FHSA, the new tax-free savings account for the purchase of a first home? We’ve gathered a wealth of information here to help you make the best decisions. FAQ, comparative table of registered plans: explore all the possibilities of this new savings product.

FHSA basics

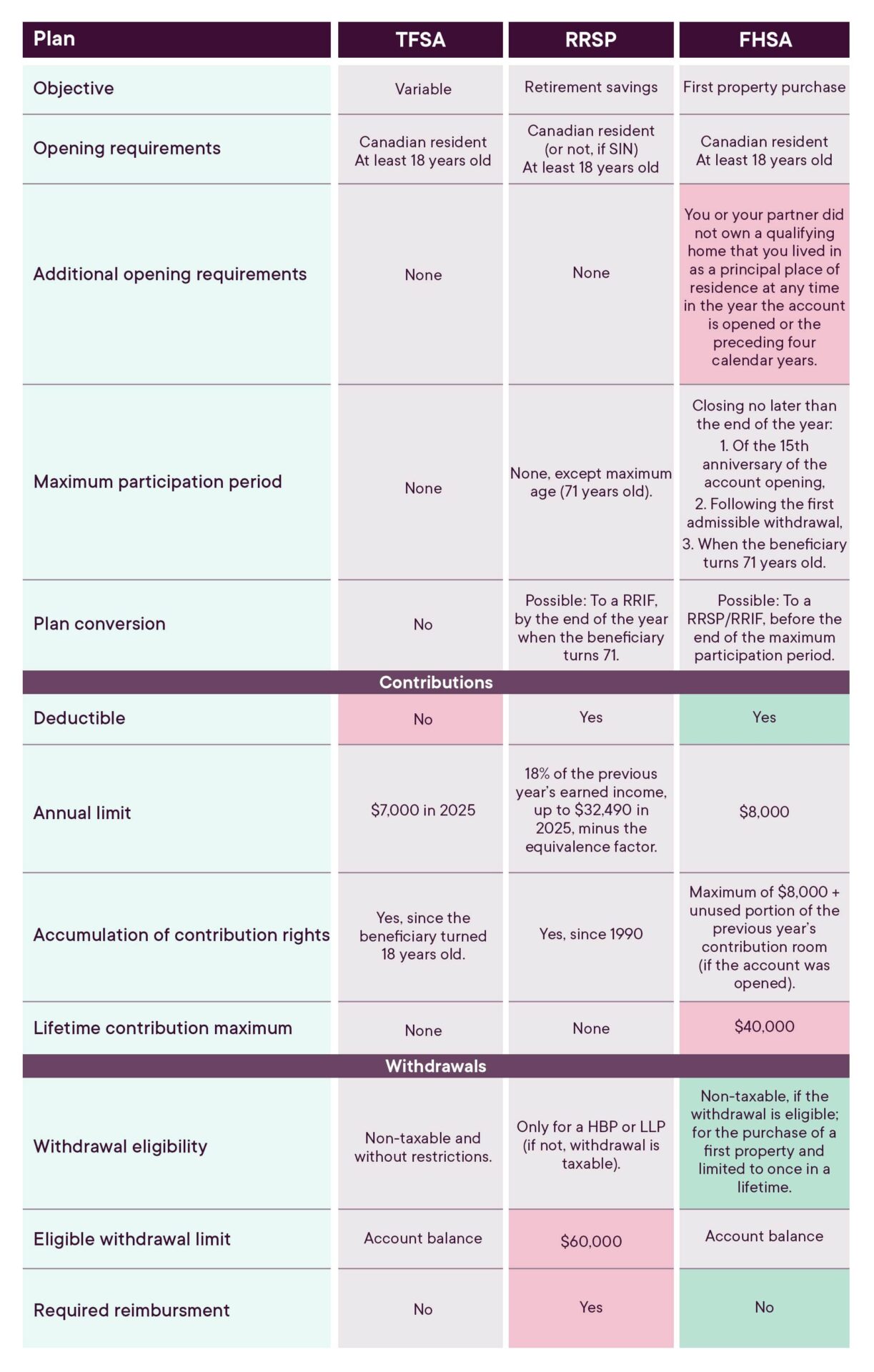

The FHSA is a savings product for Canadian residents aged 18 and over that enables them to make contributions to a tax-free registered account with a view to buying a first home.

- The maximum annual contribution to the account is $8,000.

- The maximum lifetime contribution is $40,000.

- It is possible to carry forward up to $8,000 of unused contribution room to the next year.

- Contributions made to the account are tax-deductible.

- Capital gains and interest earned in the account are non-taxable.

- Withdrawals for the purchase of a first qualifying home are also tax-free (under certain conditions) and do not have to be paid back into the account.

- The HBP and the FHSA can be used together for the down payment on a first home.

- The FHSA can remain open for a period of 15 years and must be closed either at the end of the 15th year or the year following the withdrawal for the purchase of a qualifying home.

- If not used, the amounts accumulated in the FHSA can be transferred to an RRSP when the account is closed.

If you plan to buy a home or condo, talk to your advisor. Together, you can see if the FHSA fits into your purchase plan.

Subscribe now!

Are you ready to open your FHSA account? It’s now available at fdp! Give us your contact information and an advisor from your area will quickly contact you.

Podcast

Recorded in December 2023 Published on January 8, 2024 Also available on |

Description: Saving strategically for your first home while taking advantage of a tax deduction – that’s what the new TFSA offers you. In our podcast, we’ll tell you all about the eligibility criteria for this registered plan, how it works and its many benefits. |

FAQ

Like all registered savings products, the FHSA has criteria and rules that can seem complex. Here are the most frequently asked questions, with clear and concise answers to help you understand how to use it.

Can I avail myself of both the FHSA and the HBP?

Absolutely! Although this combination wasn’t initially possible, the law now allows you to benefit from both plans, provided you meet their eligibility criteria.

Why would the FHSA be more advantageous than the HBP?

One of the great advantages of the FHSA is that a first-time home buyer does not need to repay the amounts withdrawn from their account for the purchase of their home. Also, there is no mandatory minimum holding period for the FHSA: a qualifying withdrawal can be made as soon as a contribution has been made.

Can I carry forward the deductions?

Deductions can be carried forward. In this respect, they don’t have to be claimed for the year in which a contribution was made, as with an RRSP. This allows for attractive strategies if you expect a significant increase in your income over the next few years, or substantial cash inflows.

Can I use an FHSA even if I already own a cottage?

It’s possible! You can open an FHSA if your primary place of residence is not owned by you or your spouse. So, if you usually live in an apartment and your cottage is not your main place of residence, you would be eligible for the FHSA.

Can I contribute to my spouse's FHSA?

Only the FHSA holder can contribute to their FHSA. However, you can make a gift to your spouse, who can then decide to contribute to their FHSA. However, you must comply with the rules concerning your union/legal status!

What happens if I don’t buy a home?

If the account holder has not used the accumulated funds for the purchase of a first qualifying home within 15 years of opening the account, the account must be closed. The FHSA savings can then be transferred to their RRSP without tax impact and also without reducing their RRSP contribution room.

My savings have already been used for my RRSP to take advantage of the HBP; how can I still benefit from the FHSA?

It’s possible to transfer money directly from your RRSP to your FHSA, subject to the FHSA contribution limits. In addition, this transfer will be tax-free and will not affect your RRSP contribution room!

Comparing the plans

TFSA, RRSP, FHSA: what distinguishes them? They’re all registered savings plans, but each has a specific purpose, contribution terms, tax deduction potential or not… To learn all about their features, consult our comparative table!